L’ivermectine (Stromectol) est un antiparasitaire dont l’action repose sur la liaison sélective aux canaux chlore activés par le glutamate présents dans les cellules nerveuses et musculaires des parasites. Cette fixation entraîne une augmentation du flux de chlore, provoquant une hyperpolarisation et une paralysie irréversible. L’ivermectine est active contre la gale, l’onchocercose et certaines strongyloïdoses. Sa biodisponibilité orale est variable, augmentée par la prise alimentaire, et son élimination est principalement fécale via un métabolisme hépatique. Elle ne traverse pas la barrière hémato-encéphalique, ce qui limite les effets neurologiques chez l’homme. Les précautions concernent l’interaction avec les inhibiteurs du CYP3A4, ainsi que les réactions inflammatoires dues à la destruction massive des parasites. Dans les documents de référence, stromectol prix est associé à des protocoles précis adaptés aux différentes infestations, avec une attention particulière sur la sécurité d’emploi en cas d’immunodépression.

The impact of catastrophes on shareholder value

A Research Report Sponsored by Sedgwick Group

Templeton College, University of Oxford, Oxford OX1 5NY, England

Tel +44 (0)1865 422500 Fax +44 (0)1865 422501 www.templeton.ox.ac.uk

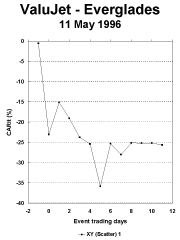

On 11 May, at around two pm Eastern time, ValuJet

by management may be redundant from the view of

DC-9 Flight 592 bound for Atlanta crashed into the

Florida Everglades soon after take-off from Miami. All passengers and crew perished. This was a human

It is too early to say what the full effect of the

catastrophe beyond comprehension. The financial

ValuJet tragedy will be on shareholder value.

consequences may also turn out to be catastrophic

However the prognosis emerging from this study is

for the relatively young airline. The study of the

bleak. ValuJet bears all the hallmarks of a "non-

financial consequences of catastrophes may seem

recoverer". Firstly, the shareholder value lost in the

morbid. However, catastrophes are phenomena

first few days was massive, amounting to about 35%

which provide a unique opportunity to evaluate how

of market capitalisation - putting it on a similar scale

financial markets respond when major risks become

to Union Carbide's Bhopal incident. Secondly, the

potential cash flow impact is enormous - probably inthe region of $308 million. Thirdly, there were a high

In formulating risk management policies, corporate

number of fatalities: all 110 passengers and crew

managers have to evaluate alternative strategies

members perished. Finally, it appears that

against the criterion of shareholder value

management will be judged to be at least partially

maximisation. Thus, a decision to hedge against

responsible for the safety lapse. All of these four

certain types of risk should hinge on whether the

factors have been identified as key determinants

value of the firm is higher or lower under hedging. In

governing the shareholder value response to

order to assess the benefits of catastrophe insurance

in value terms, a deeper insight is called for into howcatastrophes affect shareholder value and how the

This briefing aims to identify the impact of

existence of catastrophe insurance influences their

catastrophes by focusing on fifteen major corporate

impact. Preliminary findings indicate that the impact

catastrophes and tracing their impact on shareholder

of catastrophes on shareholder value is not strongly

value. As would be expected, in all cases the

influenced by the existence of catastrophe insurance.

catastrophe had a significant negative initial impact

Catastrophes appear to affect value in rather complex

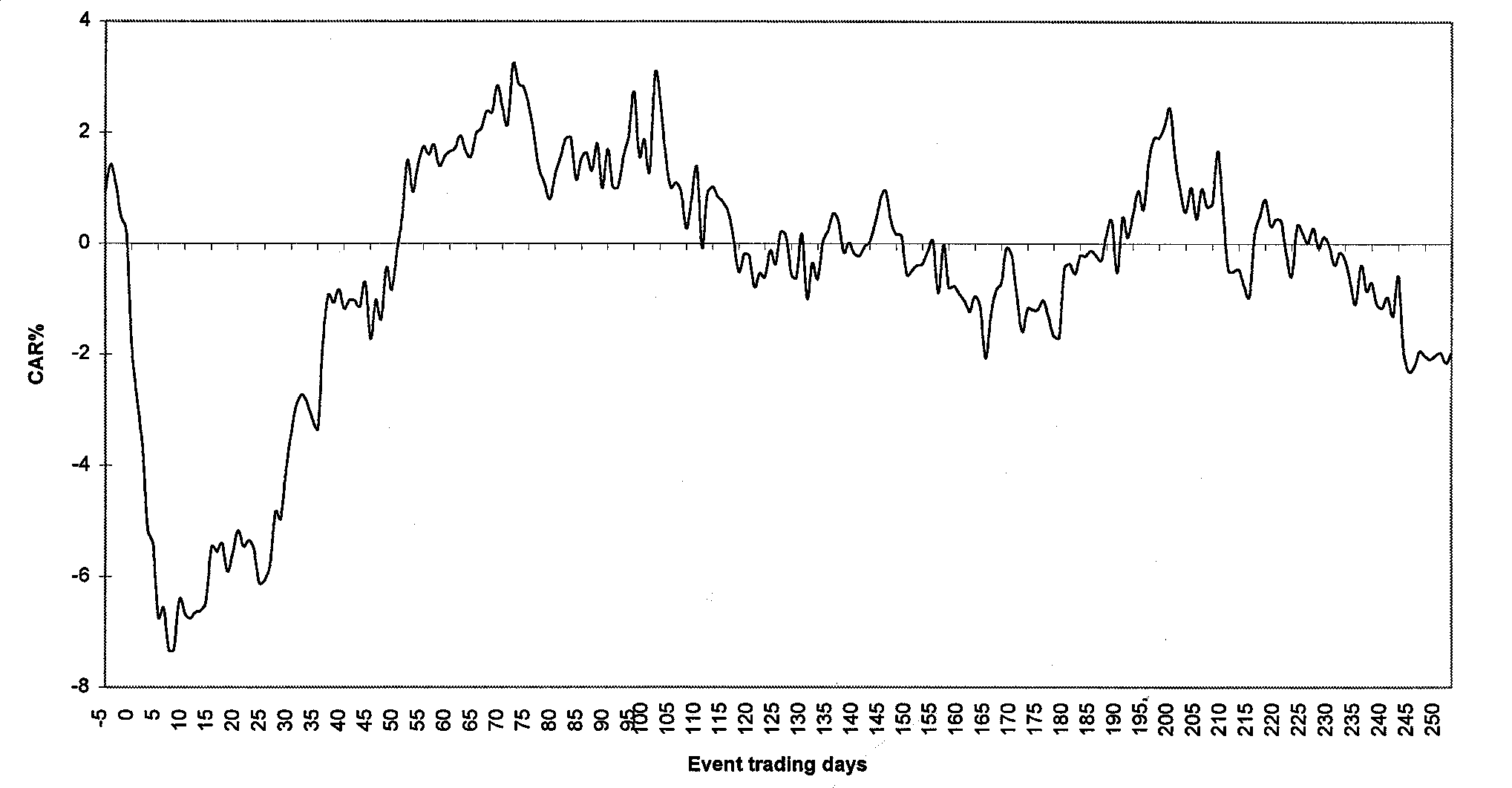

on shareholder value. Figure 1 shows the average

ways which seem to result in a re-evaluation of

impact of all the catastrophes on shareholder value.

management - which may be positive or negative.

But after a sharp initial negative impact amounting to

This result is largely consistent with modern financial

almost 8% of shareholder value, there is on average

theory which suggests that shareholder value is

an apparent full recovery in just over fifty trading

based on ex ante risk assessments in the context of

days. This suggests that the net impact on

large portfolios. In such a setting, much of the

shareholder value is negligible. However, as will be

idiosyncratic risk associated with a particular

shown below, the ability to recover the lost

company is diversified away. Further hedging of risk

shareholder value over the long-term variesconsiderably between firms.

Figure 1: Impact of Catastrophes on Shareholder Value (Full Sample)

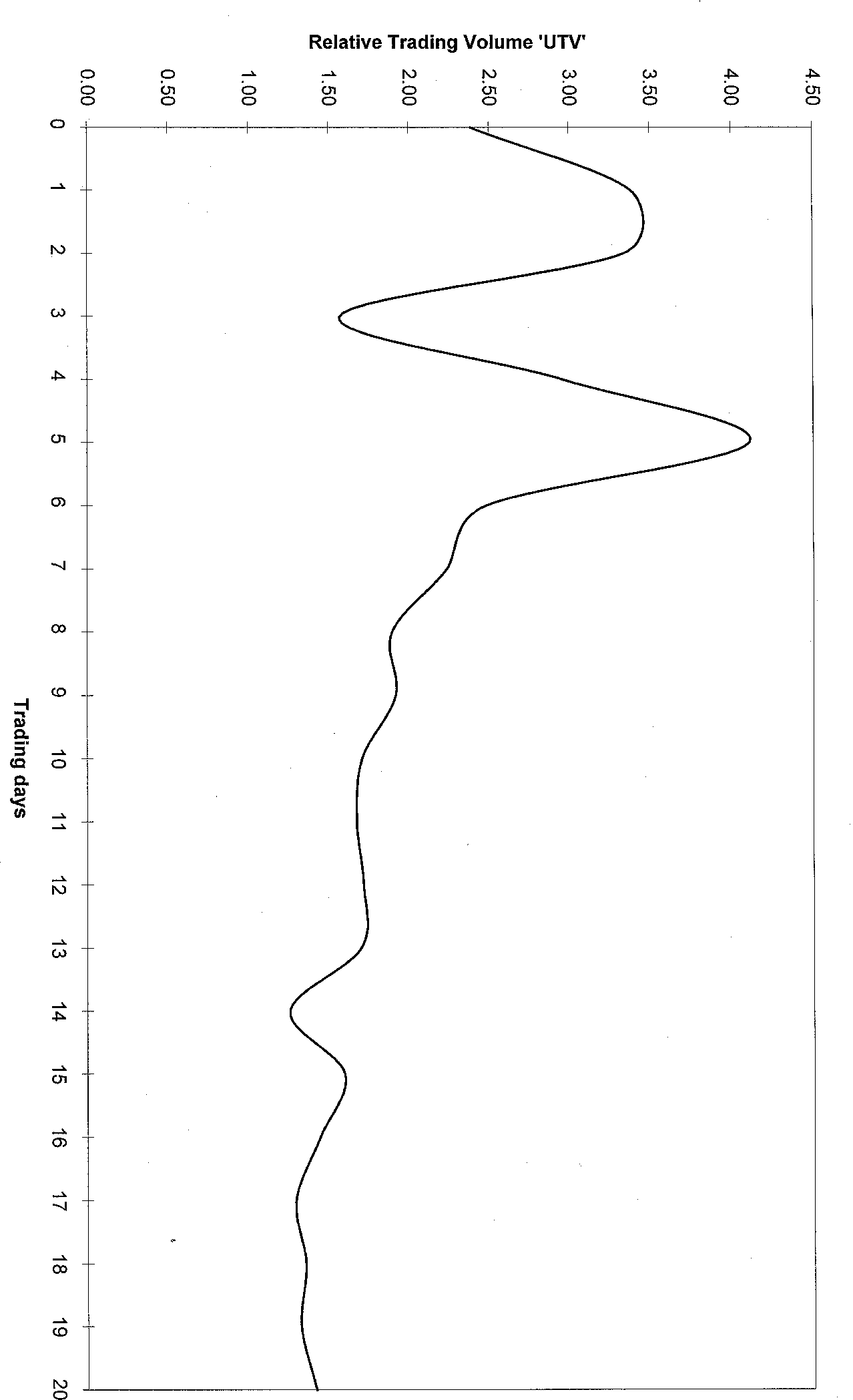

In addition to the direct impact on shareholder value,

down to normal levels around a month afterwards.

catastrophes also have a highly significant impact on

Thus, the immediate and negative impact on value

the level of trading in shares. Figure 2 shows that

not surprisingly coincides with abnormally high levels

trading in shares in these corporations is more than

of trading activity. By contrast, the drift back in

four times the usual level in the days immediately

shareholder value occurs at a normal level of trading

after the catastrophe. On average, trading settles

Figure 2: The Impact of Catastrophes on Share Trading Volume

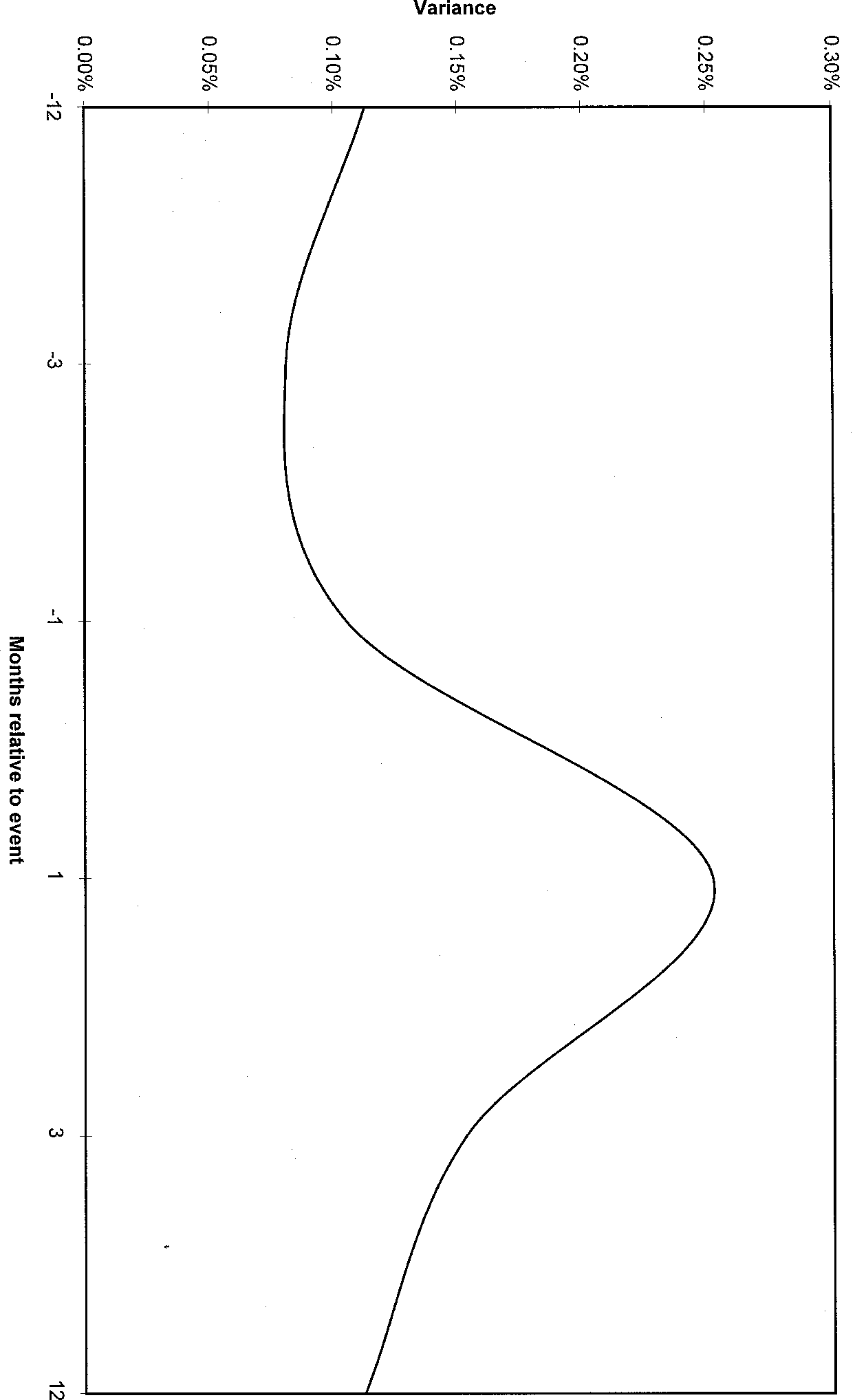

Figure 3 illustrates the impact of catastrophes on the

after the event. This result suggests that no

volatility of share returns indicating that, although

significant sustained impact on share volatility is

volatility increases initially, it does settle down soon

Figure 3: The Impact of Catastrophes on Share Volatility

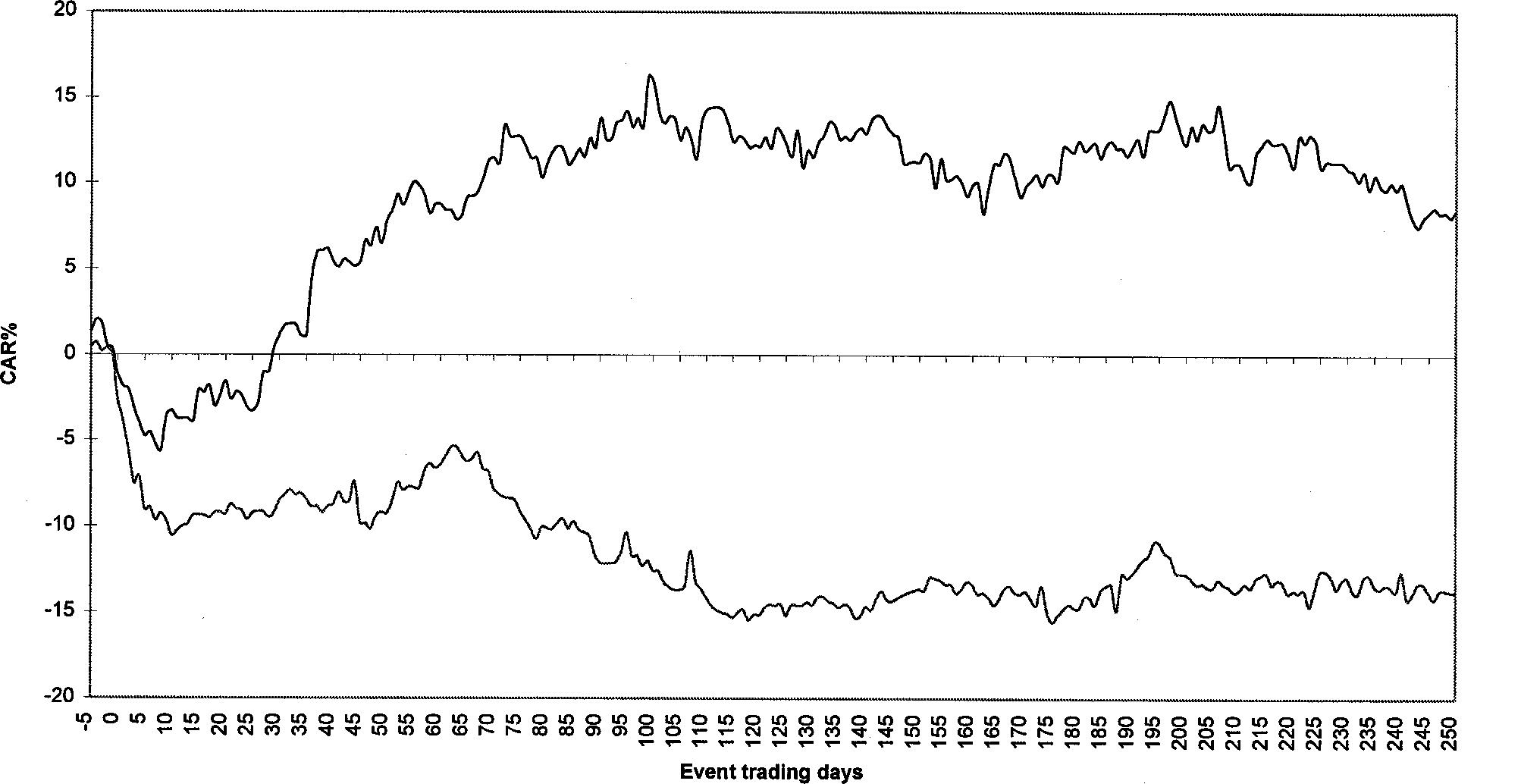

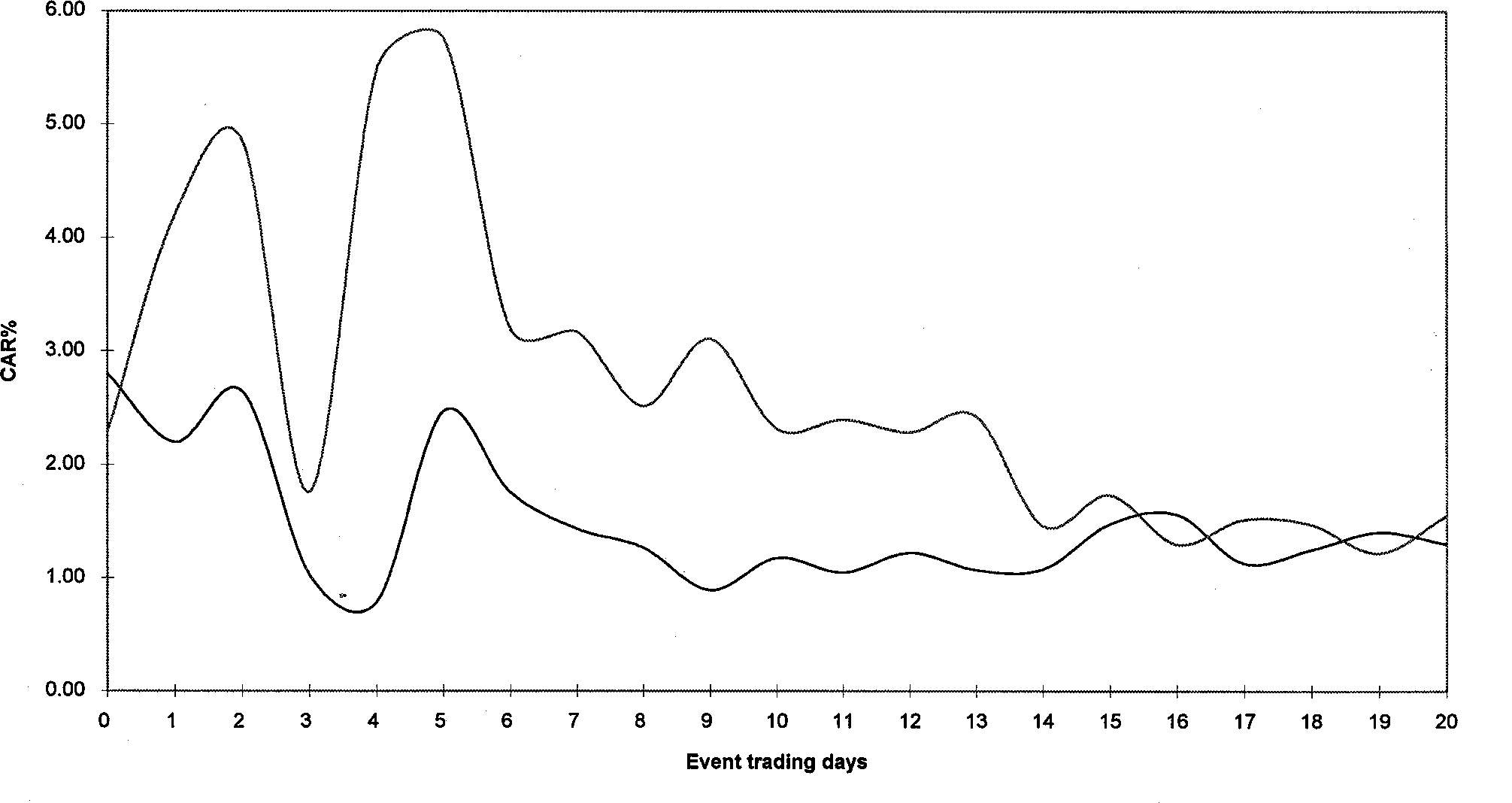

2. Why do some firms recover from loss in shareholder value better

Interestingly, firms affected by catastrophes fall into

impact on shareholder value for the recoverers was

two relatively distinct groups - recoverers and non-

5% plus. So the net impact on shareholder value by

recoverers. The initial loss of shareholder value is

this stage was actually positive. The non-recoverers

approximately 5% on average for recoverers and

remained more or less unchanged between days 5

about 11% for non-recoverers. Figure 4 shows that

and 50 but suffered a net negative cumulative impact

by the fiftieth trading day, the average cumulative

of almost 15% up to one year after the catastrophe.

Figure 5: Trading Volume of Recoverers vs Non-Recoverers

Why would some catastrophes lead to an increase in

shareholder value? One explanation from ourresearch is that there are two elements to the

catastrophic impact. The first is the immediate

estimate of the associated economic loss. Thesecond hinges on management's ability to deal withthe aftermath. Although all catastrophes have an

initial negative impact on value, paradoxically theyoffer an opportunity for management to demonstrate

their talent in dealing with difficult circumstances. Effective management of the consequences of

catastrophes would appear to be a more significantfactor than whether catastrophe insurance hedges

the economic impact of the catastrophe. Figure 5shows that the abnormal trading (shown earlier in

figure 2) is predominately caused by non-recoverers. Thus, an absence of frenetic trading around the time

of a catastrophe is usually associated with asubsequent recovery in shareholder value.

Interestingly, the research reveals that the volatilityimpact is almost identical for both recoverers and

The essential distinctions between recoverers andnon-recoverers appear to be that:

negative response of over 10% of marketcapitalisation.

In the first two or three months the magnitudeof the estimated financial loss is significant

There is a large number of fatalities. Thisseems to govern recovery in the first two or

responsibility for accident or safety lapsesappears to explain the shareholder value

By contrast, whether the losses were fully coveredby insurance does not appear to have much influence.

3. What are the implications for the insurance markets?

This research presents evidence which suggests that

The results of this study suggest that it is the

a firm's recovery of shareholder value immediately

indirect factors which dominate the impact of

following a catastrophic loss is independent of the

catastrophes on shareholder value. The net financial

presence of insurance cover. This raises interesting

loss has a relatively minor impact on the full change

issues for the consumers (companies) and the

of shareholder value associated with catastrophes.

providers (insurers and brokers) of risk managementservices.

The message is clear: catastrophe insurance cover isno protection against the shareholder value effects of

The empirical results we present suggest that the

catastrophes. This suggests that a company's

impact of a catastrophe on shareholder value derives

insurance strategy should not be considered in

from two sets of factors. The first is the direct

isolation and should not be viewed as a substitute for

financial consequences of the catastrophe. What will

high quality risk management and contingency

be the impact of the catastrophe on the firm's future

cash flows? Although the cash flow impact is notknown with certainty at the time of the catastrophe,

The results further suggest that there may be

the stock market will form a collective opinion and

considerable demand from the corporate sector for

adjust value accordingly. These direct factors will

the unbundling of traditional insurance products in

usually have a negative impact on shareholder value,

future. Frequently the insurance premium paid by a

but this impact will be cushioned by the extent to

corporate includes a fairly modest element to cover a

which insurance recoveries reduce the cash

catastrophic loss, the balance of the premium relating

to claims handling and management services. Inaddition there appear to be significant opportunities

The second set of factors are what may be described

on the supply side for the insurance providers to

as the indirect factors. These factors have an impact

expand their services in the latter end, namely by

on shareholder value which springs from what

providing more extensive risk management and

catastrophes reveal about management skills not

catastrophe management services. There appears

hitherto reflected in value. A re-evaluation of

from these results to be considerable value adding

management by the stock market is likely to result in

a re-assessment of the firm's future cash flows interms of both magnitude and confidence. This in

An unbundling of the insurance products would allow

turn would have potentially large implications for

firms to disentangle their decision to insure losses

shareholder value. Management is placed in the

from their decision to purchase risk management

spotlight and has an opportunity to demonstrate its

skill or otherwise in an extreme situation. Theindirect factors are therefore able to have a large

The results suggest that the financial loss is a small

negative or positive impact on value.

part of the value effects of a catastrophe. The crispissues facing management are:

The combined effect of the two sets of factors couldtherefore be either positive or negative: positive in

1. Is the insurance cover value for money?

circumstances where the benefits of what is revealed

2. Is there any value in outsourcing the management

about management outweigh the net financial loss of

the catastrophe; unfavourable if the revelation effectsare negative, since this will amplify the negative

The varying responses to these issues will shape the

The value of insuring the financial loss is being

1 In some circumstances the impact could be positive.

questioned seriously by many firms. What are the

For example, where the demand for a firm's products

benefits to well diversified shareholders who also

increases (with the attendant increase in cash flow)

hold shares in insurance companies? At best a zero-

as a result of consumer sympathy flowing from the

sum game perhaps? There are unlikely to be any free

catastrophe. In the context of the current

lunches on offer from the insurance industry. British

classification such effects should be defined as

Petroleum's historic decision to retain the bulk of its

indirect, ie within the second set of factors.

exposures, including catastrophe exposure, is an

been to move progressively away from a transaction-

example of this logic. Interestingly, BP management

based culture, with remuneration by brokerage,

continues to purchase risk management services

towards the provision of an increasingly wide range

from the insurance industry. The results presented

of risk management, insurance and consultancy

here seem to indicate that more corporates may

services, remunerated by fees for work undertaken

and added-value provided. These results support thewisdom of such a strategy.

Another trend evident in the last decade has been forlarge industrial corporations to adopt captive and/or

Finally, an additional response to the changing

self-insurance whilst continuing to purchase

patterns of behaviour seen recently in the commercial

catastrophe insurance cover. This is in sharp

insurance markets has been the establishment of

contrast to the BP philosophy in that these

Bermuda-based catastrophe reinsurance ventures. In

corporates have perceived value in the cover but not

1992-93 these companies attracted more than US$4

the service. This presents the insurance industry

billion of capital in the private and public markets.

with considerable opportunities and threats.

Recent years have seen also a marked growth in

Considering the results of the study it is likely that

hybrid funding mechanisms such as the catastrophe

the opportunities could be larger than the threats for

futures and options traded in Chicago. It is possible

that these new instruments will have otherramifications for post-catastrophe share price

On the supply side, the response of the global

brokers to the changes in the purchasing and riskmanagement philosophy of their major clients has

The selection of corporate catastrophes whichfollows is based on four criteria:

In addition, in each case the organisation is affected

Each involves a publicly-quoted company.

on a symbolic level as well as on a physical level. Moreover, this symbolic impact affects the whole

Each has received headline coverage in world

organisation and is not limited to a self-contained

Six of the disasters profiled were in the oil/

the results of Lloyd's of London, the largest single

petrochemical/chemical industries, and six were

provider of catastrophe insurance world-wide. Eight

product-related incidents. Overall, four events were

of the companies are American and the remaining six

attributable to deliberate acts of tampering or

are European - British, Dutch, French and Swiss.

terrorism, and in a further two sabotage was

Thus, this catastrophe portfolio is international and

suspected. Eight of the fifteen catastrophes occurred

constitutes a representative sample across industries

during the period 1988-90, which is consistent with

and across the major classes of loss world-wide.

Soon after taking off from Miami Atlanta-bound

It is believed that an employee or former employee of

ValuJet DC-9 592 crashed into the Florida

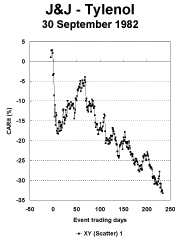

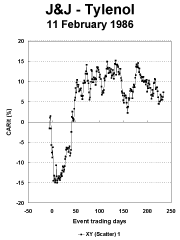

McNeilab, Inc - a unit of Johnson & Johnson -

Everglades. Although the exact cause of the crash is

injected cyanide into Tylenol (acetaminophen/

unknown, investigators believe that a fire broke outin the forward cargo hold, which was carrying aconsignment of inflammable airline oxygengenerators and tyres, and that this fire was intenseenough to break through to the passenger cabin. 110 people were killed: all 105 passengers and 5 crewmembers on board. On 13 May Standard & Poor'splaced ValuJet's "BB" corporate credit rating and"BB-" senior unsecured rating on CreditWatch withnegative implications, owing to the potential for lostpassenger revenue. On 18 May ValuJet cut itsnumber of flights - normally 320 daily - by half tocheck the safety of its aircraft. The hull value of the27-year-old DC-9 aircraft is US$4m, for which

paracetamol) extra-strength pain relieving capsules. Seven people died of cyanide poisoning; all victims inthe Chicago area. 31m bottles of Tylenol capsuleswere recalled, examined and destroyed. Sales ofextra-strength Tylenol capsules were stopped andadvertising halted. On 13 May 1991, the families ofthe seven victims reached an out-of-court settlement,the amount of which was not disclosed. On 13January 1983, Johnson & Johnson sued its insurersUS$67.4m in liability claims for the cost of recall -estimated at US$100m - and US$50m for businessinterruption losses. Johnson & Johnson insures thefirst US$5m of its product liability exposure throughits captive insurer, Middlesex Assurance Company. On 22 September 1986, a US federal judge ruled that

ValuJet is insured. It is estimated that ValuJet may

Johnson & Johnson's product liability insurance did

have to pay as much as US$300m in liability claims;

not cover the costs associated with the Tylenol

the company has liability insurance totalling

US$750m for any one occurrence. By 20 MayValuJet had refunded approximately US$4.1m topassengers whose flights were cancelled or whosetravel plans had changed as a result of the disaster. The maximum total cost of the air crash is estimatedat US$308.1m.

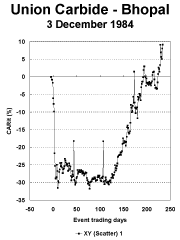

Poor safety measures, the storage of large quantities

A woman died in Bronxville, New York, after taking

of lethal gas (methyl isocyanate) at the wrong

cyanide-impregnated Tylenol (acetaminophen/

temperature, the accidental or deliberate introduction

paracetamol) capsules. On 12 February 1986, the

of water to one of the gas storage tanks, confusion in

United States suspended sales of Tylenol capsules,

detecting a rise in pressure in the tank and ineffectiveresponse to its detection - all these factors arebelieved to be responsible for the gas leak tragedy atUnion Carbide's chemical plant in Bhopal, India. Union Carbide has always refused to accept fullresponsibility for the disaster - though it accepted"moral responsibility" from the outset - maintainingthat sabotage by a disgruntled employee was themain cause of the disaster. The actual death tollfrom the Bhopal tragedy is undetermined. The mostaccurate estimate appears to be that over 3,000people died and over 300,000 were injured. About2,000 animals are estimated to have died and 7,000were injured severely. Vegetation was destroyed insurrounding areas. Many people exposed to the gaswill face a lifetime of ill-health with eye and lungdisorders. Known costs, including liability chargesand payments to build hospitals, exceed US$527m. By 12 March 1991 Union Carbide had collectedUS$167m in insurance from the disaster.

and on 3 March 1986 the sale of the drug was haltedin a further 14 countries. On 17 November 1988 aUnited States district judge ruled that neitherJohnson & Johnson nor the grocery which sold thecyanide-laced capsules was liable, and acquitted thecompanies of negligence. The cost of the recall isestimated at US$150m.

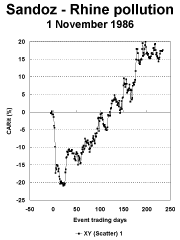

It is alleged that the fire and explosion at thechemical warehouse of Sandoz at Schweizerhalle inBasle, Switzerland was probably caused by the use ofa flame to shrink-wrap plastic covers around palletsof paint. These may have smouldered for severalhours before bursting into flame. Sandoz believesthe fire may have been the result of an arson attack. Fourteen people were injured and a cloud ofpoisonous gas was released into the atmosphere. Water used to fight the fire washed 30 tonnes oftoxic chemicals into the River Rhine, turning it red

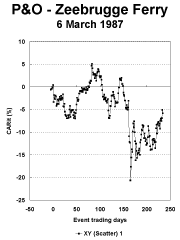

The Herald of Free Enterprise roll-on roll-off car ferrysailed from Zeebrugge harbour with its inner andouter bow doors open. It capsized and sank as adirect result of water rushing through its open bowdoors. 192 people drowned: 154 passengers and 38crew out of a total 454 passengers and 80 crew. Known legal costs total US$70m, but some activelawsuits remain.

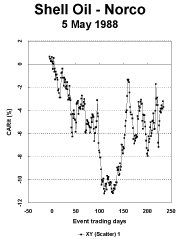

The Norco refinery and chemical plant exploded afterhydrocarbon gas escaped from a corroded pipe in a

and killing thousands of fish. Loss of the warehouseand the 800 tonnes of chemicals which were storedinside is estimated at US$12m, with an additionalUS$6m required for clean-up of the warehouse. Forthese damages Sandoz is covered by insurance. It isestimated that Sandoz will pay US$67m in liabilityclaims. The company is believed to have liabilityinsurance totalling between US$67m and US$325m.

Herald of Free Enterprise SinkingP&O, 6 March 1987

catalytic cracker and was ignited. Louisiana statepolice evacuated 2,800 residents from nearbyneighbourhoods. Seven workers were killed and 42injured. The total cost arising from the Norco blastis estimated at US$706m, comprising US$490m toreplace the cracker and US$216m in liability claims. Shell is believed to be fully insured for the event.

the bombing was ordered by Iran and the bomb was

planted by Libya with the connivance of Syria. Relatives of those killed in the crash have filed suit

At 9.45 pm on the day of the explosion one of two

against Pan Am. A few lawsuits have been settled

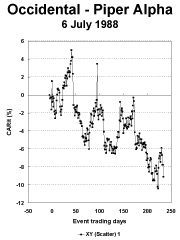

condensate injection pumps failed on the Piper Alpha

but many remain active. Following the verdictagainst Pan Am of "wilful misconduct", UnitedStates Aviation Insurance Group (USAIG) revised itsoriginal estimate of liability claims from US$250m toUS$470m in total (21 February 1994). The hull ofthe aircraft was insured for US$32m. On 21December 1989, Pan Am estimated that it hadsuffered a revenue shortfall of US$150m in lostbookings as a result of the disaster, bringing theestimated total cost to US$652m.

oil platform in the North Sea, 120 miles east of Wick,north east Scotland. The other pump had been shutdown for maintenance and, unaware of its condition,workers are assumed to have restarted it. Thisresulted in a leak of condensate, creating a smallexplosion which knocked out safety equipment, and aseries of major blasts caused a fireball. At 10.20 pm,the gas pipeline riser fractured, leading to a massiveexplosion and the collapse of the drilling derrick. 167workers died. The bodies of 31 were never

recovered. Only 63 people survived. The principal

cause of death was smoke inhalation and a few died

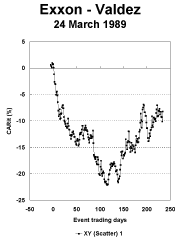

The fully loaded United States supertanker Exxon

of burns. The total financial cost of the disaster is

Valdez, ran aground in the Gulf of Alaska. It was

manoeuvering through heavy ice when it ran intoBligh Reef, puncturing 8 of its 13 cargo tanks andspilling 11m gallons of crude oil into Prince William

Sound. 1,500 miles of pristine shoreline were

polluted, more wildlife was killed than in any otherindustrial accident and Alaskan natives, particularly

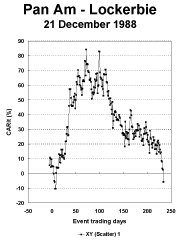

A terrorist bomb exploded aboard Pan Am Boeing

fishermen, suffered long term harm to their

747 Flight 103 causing the aircraft to crash. The

livelihoods and subsistence way of life. The latest

bomb exploded over the Scottish market town of

estimate for the total cost of the oil spill is over

Lockerbie, about 55 minutes after taking off from

US$11.5bn (7 October 1994). This figure comprises

Heathrow. 270 people were killed; all 243 passengers

US$8.7bn in damages, US$2.5bn already paid

and 16 crew on board, and 11 people on the ground.

towards the clean-up operation and US$316.5m paid

On 21 December 1993, investigations revealed that

to victims of the accident. It appears that the

International Tanker Owners Indemnity Association

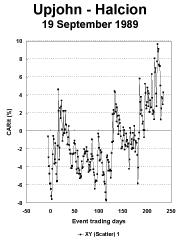

Adverse side-effects, including confusion, agitation,

provided US$400m of pollution insurance cover for

hallucinations, paranoia, amnesia and aggressive

the "Exxon Valdez" and reinsured about US$388m in

behaviour are alleged to result from taking the

Lloyd's and member companies of the Institute of

prescription drug, Halcion - Upjohn's brand-name for

benzodiazepine hypnotic triazolam. On 3 October1991, the FDA approved the drug, reporting that the"benefits outweighed its risks". Although Upjohnhas settled some cases, the company still faceshundreds of lawsuits over the drug. Marketing ofHalcion remains suspended in Britain, Norway,Argentina and Brazil. Known legal costs includethose for the "Grundberg case", a US$21m claimwhere Upjohn settled out of court for an undisclosedamount, and US$2m for a another case.

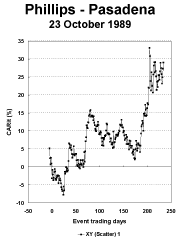

Pasadena ExplosionPhillips Petroleum, 23 October 1989

Halcion Side-EffectsUpjohn, 19 September 1989

The explosion occurred after a seal on a polyethylenereactor ruptured, leaking highly inflammable ethyleneand isobutane gas from a pipeline. It is unclear whatignited the gas. The fire blazed for more than eighthours before being brought under control and, withthe explosion, caused extensive damage to half thepetrochemical facility. 23 people were killed and 130injured. Total costs arising from the disaster areestimated at US$1,300m.

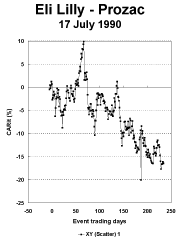

Violent secondary effects are alleged to result fromtaking the prescription anti-depressant drug, Prozac -Lilly's brand-name for fluoxetine hydrochloride. On20 September 1991, the United States federal Foodand Drug Administration (FDA) advisory committeeissued a favourable verdict on Prozac, finding no linkbetween the drug and suicide. Numerous lawsuitshave been filed against Lilly, alleging that Prozac hasdriven people to murder another, suicide and otherforms of violence. None has been successful to date,although several are still pending.

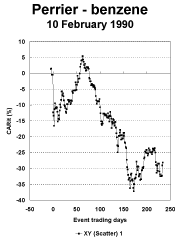

The natural gas present in the Perrier spring atVergeze in the Gard, southern France contains anumber of impurities. The carbon filters whichshould have removed these impurities, includingcancer-inducing benzene, had become clogged. Afaulty warning light on the control panel wentundetected by employees for more than six months,allowing the filters to become blocked. When themineral water was found to be contaminated bybenzene, 160m bottles were recalled from 120countries. The bottles were destroyed and replaced. Nobody suffered as a result of drinking the benzene-infected water. The Perrier group estimated that"l'incident Benzene" had cost it US$262.9m:US$197.5m for recalling and destroying the bottles,US$47.7m for related advertising communication,consultants and financial charges, and US$17.7m forassociated administration charges. Perrier did nothave product guarantee and recall insurance.

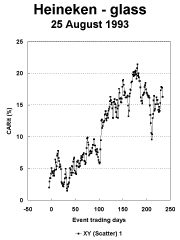

Defective glass, manufactured by BSN's VereenigdeGlas, was used to make export beer bottles. Whenopened or transported, glass splinters could fall intothe beer. Heineken recalled, destroyed and replaced15.4 million bottles. Nobody was injured as a resultof the glass splinters. At the time of occurrence,Heineken estimated the loss to be anything between$10m and $50m. It was unclear whether Heineken'sproduct liability insurance policy would cover thelosses. Coverage is unlikely, given the small marketfor product recall in Europe. On 14 April 1994Vereenigde Glas agreed to compensate Heineken foran undisclosed sum.

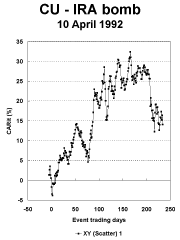

A bomb, planted by the IRA, exploded in London'sfinancial district. The 45kg bomb was placed in a caroutside the Baltic Exchange which, together with theCommercial Union (CU) tower which accommodatesthe company's headquarters, bore the brunt of theexplosion. Hundreds of CU's computers werewrecked, 2,000 panes of glass were smashed and thetower was rendered useless for a year. Three peoplewere killed and 91 injured. On 19 April 1992 totalcosts were estimated at US$2,170m, comprisingUS$560m rebuilding costs, US$560m businessinterruption claims, and US$1,050m in repairs tocomputer links, roads and a church.

In order to isolate the effect of the catastrophe on

time series regression of the return on stock i (R ) on

shareholder value, it is necessary to rule out the

the return on the market portfolio (R ). In this way,

effect of other events that may impact on shareholder

the results are controlled for market-wide influences.

value simultaneously. In this study, this isaccomplished in two phases. The first phase is at the

The abnormal returns for each firm are accumulated

individual company level and involves the filtering

out of share price movements and the effects of

market-wide factors. The result of this process is the

estimation of so-called abnormal returns for a period

immediately after the catastrophe. In the secondphase, the abnormal returns are aligned on the

catastrophe (day 0) and averaged across the total

CAR = cumulative abnormal return on portfolio p on

sample. These average abnormal returns are then

day t, relative to the day of the catastrophe (t = 0).

accumulated over what is now catastrophe time,resulting in a set of portfolio returns from day 0

N = the number of corporate catastrophes in portfolio

known as cumulative abnormal returns (CAR). The

second phase filters out any company-specific effects

In addition to examining the direct impact of the

catastrophe on shareholder value, figures 2 and 3

Figures 1 and 4 show the CARs for portfolios of the

report the impact on trading volume and volatility

total sample and the portfolios of recoverers and

respectively. The metric to evaluate the impact on

non-recoverers. The CAR charts reflect the impact

trading volume is defined relative to the average

on shareholder value in percentage terms.

More formally , the abnormal return on share i on

TV = trading volume of share i on day t.

ATV = 12 month average trading volume of share i,

over event months -6 to 0 and 1 to 7.

UTV was calculated for each share for the first

month following the event. It is assumed that

whereas a corporate catastrophe may affect stockprice behaviour throughout the entire post-event

year, any impact on trading activity will be evidentprimarily in the first post-event month only.

The expected return is modelled via a model of theform:

Volatility is measured as the volatility in the daily

share returns over a two year interval surrounding

the catastrophe. These were then averaged across

R = the return on the market portfolio on day t.

Pre-event and post-event variances were calculatedfor each catastrophe as follows:

The model parameters, a and b , represent the

intercept and slope coefficient respectively, estimated

from a market model regression of the following form:

The risk-adjustment procedure is based on the well-

n = the number of trading days in the event window.

known Capital Asset Pricing Model. The systematicrisk parameter, beta, is calculated for each individual

The raw data on share prices, trading volume and

company, and is equal to the slope coefficient in a

market capitalisation underlying this study were

market index chosen varies according to the market

obtained from the Datastream financial database.

in which the shares are traded. Since the abnormal

The data are daily and relate to trading days. The

returns on all shares are measured in real terms, their

analysis is conducted relative to a common event

additivity across numeraires appeals to Purchasing

time, rather than in calendar time. In the case of

Power Parity. Table 2 indicates the market index

each catastrophe, abnormal returns are calculated in

the local currency of the parent company, and the

Data on trading volume were unavailable for Sandoz

All other data were obtained from the annual reports

and Perrier. Consequently, the catastrophe portfolio

and accounts of the portfolio companies, and from

comprises 13 catastrophes where trading volume is

Reuters Textline, the international newspaper and

analysed. On days where there was no trading, the

data points were removed from the analysis and theaverage figures were adjusted accordingly.

1 The financial and operating results of Shell Oil Inc are

prices and trading volume were chosen to represent Shell

integrated into the consolidated accounts of Royal Dutch

Oil in the analysis. Consolidated Group figures were used in

Petroleum Company and The Shell Transport and Trading

calculations of market capitalisation.

Company plc (henceforth "Shell"), where the former owns

60% of the Group concern and Shell owns the remaining

2 Daily index figures for the Paris Bourse were unavailable.

40%. As expected, the share price behaviour of Royal

Consequently, weekly figures were used and it was assumed

Dutch and Shell were found to be highly correlated; R2 =

that the market index did not fluctuate during the week.

0.995. Consequently, for ease of data access, Shell share

Dr Knight has extensive experience of working in the

Deborah Pretty took her first degree in Industrial

financial sector. He has also held chairs in the

Economics and is now working in the field of risk

University of Cape Town and in the International

finance. Her previous experience includes risk

Management Institute, Geneva (now IMD).

management consultancy on risk retention strategies

Immediately before coming to Oxford he was the

and alternative risk finance; writing and editing risk-

Deputy Director of the Centre for Advanced Studies,

related articles for professional and trade journals;

a foundation within the Swiss National Bank (the

and involvement in corporate strategic planning,

central bank of Switzerland) - an institute with which

marketing; and risk management education and

he retains an active association. He is a visiting

training. Immediately before beginning her doctorate,

professor at a number of universities around the

she was Project Manager with Sedgwick Energy &

world including Ecole Nationale des Ponts et

Marine Limited (risk advisers and insurance brokers)

Chaussées (Paris), INSEAD (Paris), EOI (Madrid),

who are sponsoring her research. Previously, she

was a risk finance analyst with Tillinghast (actuarial

University of Cape Town. Dr Knight is also

programme director of the Oxford AdvancedManagement Programme.

Her special interests include: Corporate RiskManagement Strategy; Economics of Insurance;

His special interests include: Corporate and Financial

Alternative Risk Transfer (ART) Techniques;

Strategy; International Investments and Corporate

Strategic Planning; Risk Perception and Analysis;

Finance; Currency Risk Management; Joint Ventures;

Crisis Management; Financial Modelling.

Mergers and Acquisitions; Corporate Ownership andGovernance; International Capital and ExchangeMarkets.

LES INFILTRATIONS DEFINITION Sens strict = injections intra articulaires d’un corticoïde. Définition élargie : « infiltrations » = toutes lesinjections locales d’un dérivé corticoïde. Exclut les injections systémiques de corticoïdes : LES QUESTIONS ÿ Diagnostic au moins lésionnel. ÿ traitement validé par la communautéÿ hiérarchie thérapeutique. ÿ contre-ind

Core Content In Urgent Care Medicine GI/GU Module Release Date: December 1, 2009 Review Date: January 31, 2011 Expiration Date: November 30, 2014 Urinary Tract Infections Faculty: William Gluckman, DO, MBA, FACEP 1. The most common organism causing urinary tract infections is: a. Staph Saprophyticus b. Enterococcus c. Proteus mirabilis d. Escherichia coli 2. Whic

On 11 May, at around two pm Eastern time, ValuJet

by management may be redundant from the view of

DC-9 Flight 592 bound for Atlanta crashed into the

Florida Everglades soon after take-off from Miami.

On 11 May, at around two pm Eastern time, ValuJet

by management may be redundant from the view of

DC-9 Flight 592 bound for Atlanta crashed into the

Florida Everglades soon after take-off from Miami.

In addition to the direct impact on shareholder value,

down to normal levels around a month afterwards.

In addition to the direct impact on shareholder value,

down to normal levels around a month afterwards.

2. Why do some firms recover from loss in shareholder value better

Interestingly, firms affected by catastrophes fall into

impact on shareholder value for the recoverers was

two relatively distinct groups - recoverers and non-

5% plus. So the net impact on shareholder value by

recoverers. The initial loss of shareholder value is

this stage was actually positive. The non-recoverers

approximately 5% on average for recoverers and

remained more or less unchanged between days 5

about 11% for non-recoverers. Figure 4 shows that

and 50 but suffered a net negative cumulative impact

by the fiftieth trading day, the average cumulative

of almost 15% up to one year after the catastrophe.

2. Why do some firms recover from loss in shareholder value better

Interestingly, firms affected by catastrophes fall into

impact on shareholder value for the recoverers was

two relatively distinct groups - recoverers and non-

5% plus. So the net impact on shareholder value by

recoverers. The initial loss of shareholder value is

this stage was actually positive. The non-recoverers

approximately 5% on average for recoverers and

remained more or less unchanged between days 5

about 11% for non-recoverers. Figure 4 shows that

and 50 but suffered a net negative cumulative impact

by the fiftieth trading day, the average cumulative

of almost 15% up to one year after the catastrophe.

Soon after taking off from Miami Atlanta-bound

It is believed that an employee or former employee of

ValuJet DC-9 592 crashed into the Florida

McNeilab, Inc - a unit of Johnson & Johnson -

Everglades. Although the exact cause of the crash is

injected cyanide into Tylenol (acetaminophen/

unknown, investigators believe that a fire broke outin the forward cargo hold, which was carrying aconsignment of inflammable airline oxygengenerators and tyres, and that this fire was intenseenough to break through to the passenger cabin.

Soon after taking off from Miami Atlanta-bound

It is believed that an employee or former employee of

ValuJet DC-9 592 crashed into the Florida

McNeilab, Inc - a unit of Johnson & Johnson -

Everglades. Although the exact cause of the crash is

injected cyanide into Tylenol (acetaminophen/

unknown, investigators believe that a fire broke outin the forward cargo hold, which was carrying aconsignment of inflammable airline oxygengenerators and tyres, and that this fire was intenseenough to break through to the passenger cabin.

Poor safety measures, the storage of large quantities

A woman died in Bronxville, New York, after taking

of lethal gas (methyl isocyanate) at the wrong

cyanide-impregnated Tylenol (acetaminophen/

temperature, the accidental or deliberate introduction

paracetamol) capsules. On 12 February 1986, the

of water to one of the gas storage tanks, confusion in

United States suspended sales of Tylenol capsules,

detecting a rise in pressure in the tank and ineffectiveresponse to its detection - all these factors arebelieved to be responsible for the gas leak tragedy atUnion Carbide's chemical plant in Bhopal, India.

Poor safety measures, the storage of large quantities

A woman died in Bronxville, New York, after taking

of lethal gas (methyl isocyanate) at the wrong

cyanide-impregnated Tylenol (acetaminophen/

temperature, the accidental or deliberate introduction

paracetamol) capsules. On 12 February 1986, the

of water to one of the gas storage tanks, confusion in

United States suspended sales of Tylenol capsules,

detecting a rise in pressure in the tank and ineffectiveresponse to its detection - all these factors arebelieved to be responsible for the gas leak tragedy atUnion Carbide's chemical plant in Bhopal, India.

The Herald of Free Enterprise roll-on roll-off car ferrysailed from Zeebrugge harbour with its inner andouter bow doors open. It capsized and sank as adirect result of water rushing through its open bowdoors. 192 people drowned: 154 passengers and 38crew out of a total 454 passengers and 80 crew.

The Herald of Free Enterprise roll-on roll-off car ferrysailed from Zeebrugge harbour with its inner andouter bow doors open. It capsized and sank as adirect result of water rushing through its open bowdoors. 192 people drowned: 154 passengers and 38crew out of a total 454 passengers and 80 crew.

the bombing was ordered by Iran and the bomb was

planted by Libya with the connivance of Syria.

the bombing was ordered by Iran and the bomb was

planted by Libya with the connivance of Syria.

International Tanker Owners Indemnity Association

Adverse side-effects, including confusion, agitation,

provided US$400m of pollution insurance cover for

hallucinations, paranoia, amnesia and aggressive

the "Exxon Valdez" and reinsured about US$388m in

behaviour are alleged to result from taking the

Lloyd's and member companies of the Institute of

prescription drug, Halcion - Upjohn's brand-name for

benzodiazepine hypnotic triazolam. On 3 October1991, the FDA approved the drug, reporting that the"benefits outweighed its risks". Although Upjohnhas settled some cases, the company still faceshundreds of lawsuits over the drug. Marketing ofHalcion remains suspended in Britain, Norway,Argentina and Brazil. Known legal costs includethose for the "Grundberg case", a US$21m claimwhere Upjohn settled out of court for an undisclosedamount, and US$2m for a another case.

International Tanker Owners Indemnity Association

Adverse side-effects, including confusion, agitation,

provided US$400m of pollution insurance cover for

hallucinations, paranoia, amnesia and aggressive

the "Exxon Valdez" and reinsured about US$388m in

behaviour are alleged to result from taking the

Lloyd's and member companies of the Institute of

prescription drug, Halcion - Upjohn's brand-name for

benzodiazepine hypnotic triazolam. On 3 October1991, the FDA approved the drug, reporting that the"benefits outweighed its risks". Although Upjohnhas settled some cases, the company still faceshundreds of lawsuits over the drug. Marketing ofHalcion remains suspended in Britain, Norway,Argentina and Brazil. Known legal costs includethose for the "Grundberg case", a US$21m claimwhere Upjohn settled out of court for an undisclosedamount, and US$2m for a another case.

Violent secondary effects are alleged to result fromtaking the prescription anti-depressant drug, Prozac -Lilly's brand-name for fluoxetine hydrochloride. On20 September 1991, the United States federal Foodand Drug Administration (FDA) advisory committeeissued a favourable verdict on Prozac, finding no linkbetween the drug and suicide. Numerous lawsuitshave been filed against Lilly, alleging that Prozac hasdriven people to murder another, suicide and otherforms of violence. None has been successful to date,although several are still pending.

Violent secondary effects are alleged to result fromtaking the prescription anti-depressant drug, Prozac -Lilly's brand-name for fluoxetine hydrochloride. On20 September 1991, the United States federal Foodand Drug Administration (FDA) advisory committeeissued a favourable verdict on Prozac, finding no linkbetween the drug and suicide. Numerous lawsuitshave been filed against Lilly, alleging that Prozac hasdriven people to murder another, suicide and otherforms of violence. None has been successful to date,although several are still pending.

Defective glass, manufactured by BSN's VereenigdeGlas, was used to make export beer bottles. Whenopened or transported, glass splinters could fall intothe beer. Heineken recalled, destroyed and replaced15.4 million bottles. Nobody was injured as a resultof the glass splinters. At the time of occurrence,Heineken estimated the loss to be anything between$10m and $50m. It was unclear whether Heineken'sproduct liability insurance policy would cover thelosses. Coverage is unlikely, given the small marketfor product recall in Europe. On 14 April 1994Vereenigde Glas agreed to compensate Heineken foran undisclosed sum.

Defective glass, manufactured by BSN's VereenigdeGlas, was used to make export beer bottles. Whenopened or transported, glass splinters could fall intothe beer. Heineken recalled, destroyed and replaced15.4 million bottles. Nobody was injured as a resultof the glass splinters. At the time of occurrence,Heineken estimated the loss to be anything between$10m and $50m. It was unclear whether Heineken'sproduct liability insurance policy would cover thelosses. Coverage is unlikely, given the small marketfor product recall in Europe. On 14 April 1994Vereenigde Glas agreed to compensate Heineken foran undisclosed sum.