L’ivermectine (Stromectol) est un antiparasitaire dont l’action repose sur la liaison sélective aux canaux chlore activés par le glutamate présents dans les cellules nerveuses et musculaires des parasites. Cette fixation entraîne une augmentation du flux de chlore, provoquant une hyperpolarisation et une paralysie irréversible. L’ivermectine est active contre la gale, l’onchocercose et certaines strongyloïdoses. Sa biodisponibilité orale est variable, augmentée par la prise alimentaire, et son élimination est principalement fécale via un métabolisme hépatique. Elle ne traverse pas la barrière hémato-encéphalique, ce qui limite les effets neurologiques chez l’homme. Les précautions concernent l’interaction avec les inhibiteurs du CYP3A4, ainsi que les réactions inflammatoires dues à la destruction massive des parasites. Dans les documents de référence, stromectol prix est associé à des protocoles précis adaptés aux différentes infestations, avec une attention particulière sur la sécurité d’emploi en cas d’immunodépression.

Fgcasal.org

PRICE COMPETITION IN PHARMACEUTICALS: THE CASE

A fundamental question in industrial organization regards the relationship between

price and the number of sellers. This relationship has been particularly important in the

pharmaceutical industry where legislative changes were specifically designed to foster

competition. Previous research on the pharmaceutical industry has shown generic entry

has a mixed impact; generic prices fall rapidly with generic entry, whereas branded

prices tend to increase or decrease only slightly. Using more complete data, focused on

one segment of the pharmaceutical industryÐanti-infectivesÐwe find that the

relationship between pharmaceutical prices and the number of sellers is more like

that found in other industries. (JEL L11, L65, D4)

between 6 and 15, and fall by another 52% as

sellers increase from the 6 to 15 range to more

organization regards the relationship between

than 40. These results contrast with previous

price and the number of sellers (N ). The inter-

work on pharmaceuticals using more limited

est in this issue has been rekindled by substan-

data and showing little impact of entry on

tial recent work.1 This article uses an extensive

branded prices.4 The results here indicate

data set to provide an empirical analysis of the

instead that the effect of an increase in number

price±N relationship for antiinfective pharma-

of sellers on prices in pharmaceuticals is similar

ceutical products.2 The analysis shows that (1)

prices fall rapidly moving from one seller to a

few and (2) subsequent increases in the number

attracted scrutiny from both policy makers

of sellers continue to reduce prices, even when

there are numerous sellers.3 Prices fall about

have been a number of studies of pharmaceu-

83% as the number of sellers increases from 1 to

tical pricing behavior in general and the impact

of generic entry on branded and generic drug

prices in particular. Most of the previous stud-

*We thank Michael Baye, Dean Lueck, and seminar

ies have concentrated on small sets of drugs

participants at Chicago, LSU, Penn State, Texas A&M,

that have faced patent expiration across a num-

UCLA, the University of Texas, and the spring 1994 meet-

ings of the Industrial Organization Group of the NBER for

ber of therapeutic classes. Early studies focused

helpful comments. Financial support from Merck & Co.

on reduced form or semireduced form regres-

sion models that showed that branded prices

Wiggins: Professor, Department of Economics, Texas

and generic prices responded differently to

A&M University, College Station, TX 77843-4228.

Phone 1-979-845-7351, Fax 1-979-847-8757, E-mail

generic entry. In particular, these studies

showed that branded prices responded little

Maness: Senior Managing Economist, LECG, LLC, 2700

Earl Rudder Frwy., Suite 4800, College Station, TX

77845. Phone 1-979-694-5780, Fax 1-979-694-2442,

4. The analysis here builds on Caves et al. (1991) and

Grabowski and Vernon (1992) but covers a much larger set

of products, including all 98 in the anti-infective category.

1. See, for example, Applebaum (1982), Bresnahan

In contrast, Caves and colleagues used 30 products and

(1981), Bresnahan and Reiss (1991), Caves et al. (1991),

Grabowski and Vernon used only 18. Later studies also

Porter (1993), Reiss and Spiller (1989), and Suslow

use limited numbers of products. Frank and Salkever

(1986); portions of this literature are summarized in

(1997) have a sample of 45 drugs; Reiffen and Ward

(2002) uses 32 drugs. By using a larger number of products

2. Although our analysis concentrates on the relation-

concentrated in a single therapeutic category, we hope to

ship between price and the number of firms, there has also

determine how prices are affected by the number of sellers

been substantial work on the relationship between price

for an entire group of products and avoid thorny problems

associated with the heterogeneities in product use. The

3. It should be noted that there is little if any price effect

analysis here also provides a much more in-depth evalua-

when the second generic enters, but price effects become

tion of the competition between branded and generics not

significant as the third and fourth generics enter.

found in these earlier investigations.

# Western Economic Association International

to generic entry, and in some studies even

primarily treat acute conditions, and a single

increased (see Caves et al., 1991; Grabowski

prescription is usually enough to treat a condi-

and Vernon 1992; 1996). Frank and Salkever

tion, prescriptions make a natural measure of

(1992) developed a theoretical model to explain

quantity. However, anti-infectives are some-

the anomaly of rising branded prices in the face

what different from other therapeutic cate-

of generic competition. Their model posited

gories in that generic entry has historically

a segmented market where there existed two

been less costly than in other categories. The

segment that continues to buy the established

branded product after generic entry and a

price-conscious segment. Frank and Salkever

approval of generic products, had essentially

show that because of the segmented nature of

been in place for decades for anti-infectives. As

the market, entry likely makes the demand

a result, although other categories did not see

facing the branded manufacturer less elastic

substantial generic entry until after 1984, anti-

infectives had faced numerous generic entrants

and Salkever (1997) provide empirical tests and

for some time. In addition, many anti-infective

confirm that, consistent with the segmented

products, especially older ones, tend to be pre-

markets theory, branded prices rise and generic

scribed by generic name instead of the brand

prices fall in response to generic entry.

name, which hastens the acceptance of generic

Finally, a number of studies have attempted

to characterize the behavior of generic firms.

These factors have led some researchers to

Scott Morton (1999; 2000) finds that revenue in

predict that branded anti-infective prices may

the years before patent expiration is the most

respond differently from those in other cate-

important determinant of how many generic

gories. Early empirical research seemed to con-

firms enter a given market. She also finds

firm that result.7 Later empirical research has

that generic firms tend to specialize in certain

provided more mixed results, with some studies

showing a pattern of rising branded anti-

infective prices in the face of generic entry.8

response of generic prices to generic entry.

Our results are more in line with the earlier

This article investigates how prices decline

studies, showing significant impact on branded

as the number of sellers rises, evaluating the

ability of formal theoretical models to organize

A second difference in our data is that they

the data. The results show that although exist-

measure activity at the retail level. The use of

ing models organize some of the data regarding

retail prices raises two issues for our analysis.

price declines, there are important discrepan-

Previous research has pointed out that phar-

cies between the data and existing models.

macists may have a financial incentive to favor

We then characterize the differences between

generic dispensing, especially since the advent

the data and the models, providing a basis for

of managed care (see Grabowski and Vernon

continued theoretical and empirical work.

1996). However, our data end in 1990, when

There are a number of important differences

managed care was a much smaller factor than it

between the data we use and those of previous

is today. A second issue is to what extent retail

researchers. First, unlike previous research

prices can be used to analyze price competi-

tion among manufacturers. Given the intense

focused on a single therapeutic categoryÐ

anti-infectives. This focus on a single therapeu-

tic category provides a number of benefits,

drugs. See Lu and Comanor (1998), Scott Morton (1999,

particularly with regard to controlling for

6. Such acceptance may also occur because the U.S.

cost differences and demand differences.

Food certifies the manufacture of each batch of active

Anti-infectives in particular is a useful category

ingredient for anti-infectives, but not necessarily for

because they are primarily used for acute con-

ditions, thus making demand conditions more

7. See in particular, Schwartzman (1976, chapter 12).

See also Congressional Budget Office (1998, chapter 3).

uniform.5 In addition, because anti-infectives

8. Both Ellison (1998), and Griliches and Cockburn

(1994) find that average branded anti-infective prices

rise with generic entry, whereas Ellison et al. (1997) find

5. Several studies note that the demand and supply

significant responsiveness between branded and generic

conditions may be different for acute versus chronic

WIGGINS & MANESS: PRICE COMPETITION IN PHARMACEUTICALS

competition among retail pharmacies, and the

data are used to construct an annual price per

use of simple pricing rules that apply across

prescription for each seller of each product

most (if not all) drugs, price competition

(detailed data appendix available on request).

among manufacturers is likely to be reflected

Attention is restricted to anti-infectives to con-

trol for units of measure, cost, and regulatory

conditions across products. Doctors normally

econometric analyses of product differentia-

write an anti-infective prescription for a quan-

tion, including identifying separate effects on

tity of medication designed to cure a given

prices from increases in both generic and brand

infection. This practice makes the individual

name competition. This analysis of competi-

prescription the natural unit of measure for

tion between branded and generic products

anti-infectives. For other pharmaceuticals, in

shows (1) that it is important to distinguish

contrast, a pill or a daily dose might be more

between branded products sold by other inno-

relevant.11 The active ingredients for these pro-

vative firms besides the pioneer and unbranded

ducts are also commonly manufactured using

entry by traditional generic manufacturers; (2)

identical equipment, making costs more similar

branded entry by other innovative firms has a

for anti-infectives than across pharmaceuticals

different effect on pioneer prices than generic

as a whole. Still, the analysis that follows intro-

entry by strictly off-brand firms; and (3) there

duces several control variables to allow for cost

appears to be significant competition between

differences in a more sophisticated way than in

generic and brand-name sellers, including the

pioneer. Hence the results indicate that there

are three distinctive product groups in pharma-

review standards are also the same within this

ceuticals: the pioneer, branded versions of the

class of products, so that regulatory costs and

same molecule sold by other innovative firms,

standards are also similar. Hence cost differ-

and ordinary generics, and there is significant

ences are likely small, and we can control

price competition within and between these

adequately for different manufacturing tech-

niques for different groups of products (see

We briefly review some summary statistics,

a complete review is available in the data

appendix (available on request). The average

The data consist of retail-level pharmacy

price (1982±84 dollars) in the sample is $10.29

transaction data for all anti-infective products

with a standard deviation of $21.68. The smal-

over the 1984±90 period.10 The data provide

lest price is 0 and the largest price is $391.46.13

yearly observations on total expenditures

and quantity of prescriptions sold for the indi-

vidual sellers of anti-infective products. These

11. It should be noted that there may be different dos-

ing and different presentations, e.g. liquid versus tablet, but

that regardless of the dosing or presentation the standard

practice is to write a prescription to cure the infectionÐ

9. The IMS data we use for our empirical analysis do

which is why physicians tenaciously encourage patients to

not include rebates that are commonly paid by branded

manufacturers to managed care. Congressional Budget

12. The analysis introduces dummy variables for

Office (1998) notes that these rebates can continue and

each class of productsÐfor example, tetracyclines and

increase after generic entry, and thus not measuring

penicillinsÐand also uses separate dummy variables for

them can obscure an important source of price competition

year of introduction that allows a flexible, nonparametric

for branded manufacturers. Note, however, that wholesale

estimation of possible trends or other changes in cost over

level data from IMS possess the same weakness, and to the

time, reflecting increased complexity due to more sophis-

extent that such rebates are important, our results under-

ticated molecules or changes in manufacturing techniques.

estimate the degree to which branded manufacturers

These controls represent a significant improvement over

previouswork(see,e.g.,Cavesetal.1991,whouseadummy

10. The data were obtained from the National Pre-

variable by therapeutic class, which would be the same as

scription Audit of IMS America. Total expenditures and

imposing constant costs for all products in our sample).

quantity data are collected from a stratified random sample

13. The reader should note that there are seven obser-

of pharmacies and then used to construct nationwide retail

vations where total revenue is reported as zero and several

sales estimates. In the present analysis, these monthly data

observations where revenue is also extraordinarily high,

have been aggregated into annual series, forming a panel

both yielding outliers in pricing calculations. Reestimation

data set where the unit of observations are annual data for

without these observations does not qualitatively change

an individual product sold by an individual company.

The average branded price (constant dollars) is

$30.30 with a standard deviation of $45.77, and

the average generic price (constant dollars) is

$6.27 with a standard deviation of $6.91. The

number of sellers for a given product varies

from 1 (monopoly) to 61. The mean is 26.9

sellers. Our measure for the number of related

sellers has a mean of 31.6 and ranges between

0 and 112. We also calculated the Herfindahl

entity in each year. The mean HHI in the sam-

ple is 3,677, and the standard deviation is 2,669.

brand-name products, 13% are pioneer pro-

ducts. The number of observations is fairly

evenly spread across the sample period and

across IMS classifications. Erythromycins

(14%) and cephalosporins (9.6%) contain the

Almost half the observations (46%) are from

drugs introduced before 1962. In other years,

introductions vary from none in some years up

to 8.4% of the sample in 1974. Thus the data set

provides much detail and ample variation for

Anti-infective products are broadly catego-

rized according to the general molecular struc-

ture of the central active chemical entity, such

as penicillins, tetracyclines, erythromycins,

further disaggregated into specific molecular

entities or combinations, and the analysis

here focuses on the number of sellers of these

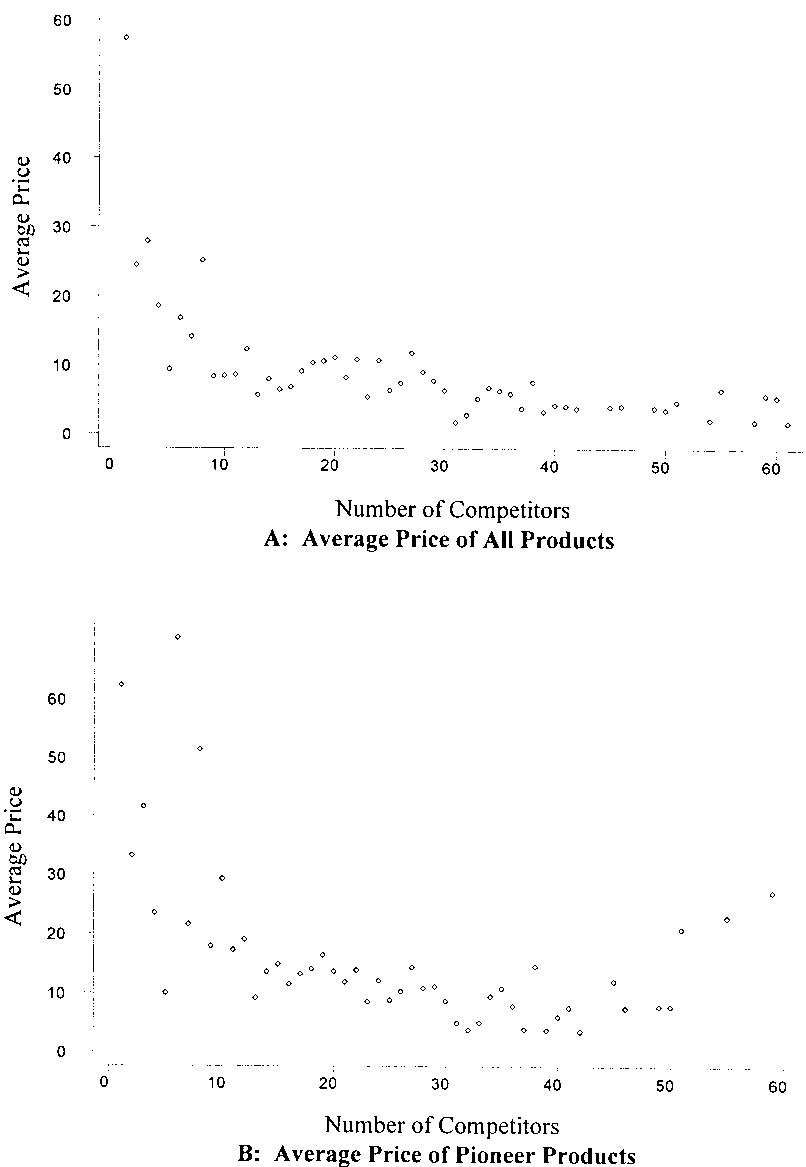

The first point on the horizontal axis corre-

individual products. Our data include 98 sepa-

sponds to drugs with one seller and the price

rately identified compounds. The analysis also

is averaged over all such products in the

considers competition among sellers of closely

sample, the second price is the average price

related molecules. Ellison et al. (1997) examine

for all two-seller drugs, and so forth.14

cross-product price competition in cephalo-

Figure 2 presents a similar view using HHI

sporins, and find mixed evidence of price com-

petition across products for these closely

The two panels of Figure 1 present two dif-

related antibiotics. In contrast, Stern (1994)

ferent looks at the data. A shows average prices

finds that in two of his four categories there

for all sellers, and B shows the average price for

is significant intermolecular substitution.

just the pioneersÐthe firms that originally

Accordingly, in the econometrics we allow

for intermolecular effects, though our results

drop in prices with the entry of the second

are more similar to Ellison et al. than to Stern.

through fifth sellers. Prices fall from the single

seller price of more than $57 to $9.46 when

metric specification, however, it is valuable

there are five sellers. This rapid decline in prices

to examine the simple relationship between

continues throughout most of the relevant

price and number of sellers. Figure 1 presents

these data. Although the econometric analysis

uses individual prices for each seller in a panel

14. With 98 product categories and 7 years of data,

data set, for clarity Figure 1 simply presents

there are 686 possible industry concentration outcomes.

average prices, taking the mean price of all

For example, there are 178 monopolies and 45 duopolies

(90 price observations) making up the first two points in

drugs with a particular number of sellers.

WIGGINS & MANESS: PRICE COMPETITION IN PHARMACEUTICALS

Prices of Products and Number of Competitors

range. B, focusing just on the prices of the pio-

continuing price decline in the reduced form

neer developer, shows essentially the same

that continues from only a few sellers to more

pattern. Hence, these data show a decline in

than 40. Focusing just on the pioneer pro-

both overall average prices and prices of the

We tried other specifications, and all the

The continuing price decline is well illus-

results are broadly similar. For instance,

trated through a series of simple regressions of

although our analysis concentrates on the

the price±N relationship, with progressive

price±N relationship, we also calculated

truncation of the sample on N from the left-

the HHI for each of our 98 chemicals. The

hand side. These regressions permit one to

mean HHI was 3,677 with a standard deviation

assess the persistence of the inverse relation-

of 2,669. The range was 1,082 to 10,000. After

ship between price and N. The results show

constructing the HHI, we then replicated the

that there is a statistically significant impact

regressions using the HHI in place of the num-

of the number of sellers on price, including

ber of firms. We ran a series of regressions,

when the sample is restricted to more than

30 sellers.15 Hence there is a significant,

16. It should be noted that there is a single outlier for

the pioneer products, which makes some difference in the

15. The coefficient on the number of sellers in the sim-

results. There appear to be data problems with the prices

ple price±N truncated regressions are as follows (t-statistics

for this drug, Vibramycin (PFizer: the pioneer doxy-

in parentheses): for regressions including all chemicals

cycline). If Vibramycin is included, the effect of N is insig-

(N b 0), b À0.47 (À21.42); for the regressions including

nificant for N ! 20, and significant and positive for N ! 30.

only chemicals with five or more competitors (N ! 5),

With Vibramycin removed, the result is a significant nega-

b À0.15 (À14.213); for N ! 10, b À0.13 (À14.46); for

tive coefficient for N ! 20 and negative but insignificant for

N ! 20, b À0.15 (À13.38); N ! 30, b À0.06 (À3.81);

N ! 30. We have not found other instances where Vibra-

mycin swings results in this way or other similar outliers.

truncating the Herfindahl from above. The

To formalize the Cournot prediction, sup-

coefficient remained positive and significant,

even when the regression was restricted to a

P(Q) a À bQ with constant marginal cost,

HHI of less than 2,000. Thus, decreasing con-

c ` a, and where Q represents total market

centration reduces price, even for chemicals

output. With N identical sellers, the market

price generated by the Cournot model takes

It is unlikely that manufacturing cost differ-

ences explain the observed differences in price.

Anti-infectives appear to exhibit constant

marginal production costs, and manufactur-

ing techniques are highly similar. There are

differences in presentation, such as tablets,

Note that the Cournot model predicts a linear

capsules, and suspensions, but these differ-

relationship between price and roughly the

ences cut across products and groups of pro-

could make a large, systematic difference is

equation (1) when there is a linear demand

for intravenous drugs, which we investigate

and constant marginal cost. Constant cost is

later. Hence manufacturing cost differences

highly plausible for anti-infectives because the

are unlikely to explain observed price differ-

raw ingredients are manufactured in batches

ences. Still it is important to control carefully

that are small relative to total output and pill

making is constant cost. Linearity of demand,

might affect the observed price±N relation-

however, is a stronger assumption suggesting

ship, requiring a more detailed econometric

that one can think of (1) as a Cournot-like out-

come rather than a structural test (see later

The Cournot model also assumes that firms

are identical. For many of the chemicals in our

analysis, especially those that have been off

patent for a number of years, this assumption

relationship between price and the number of

is plausible. The industry uses batch produc-

sellers, it is useful to rely on formal models to

tion technology characterized by constant

guide the analysis. The data summarized in

returns to scale. For this reason, most of the

Figure 1 show a continuous decline in price,

previous literature in the field also uses

ruling out a simple Bertrand model of price

the number of competitors as the key variable

competition. Recognizing this, two simple

determining the competitiveness of prices

alternative models of competition are the stan-

(see Stern 1994; Ellison et al. 1997 for instance).

Though the results reported use the number of

the entry threshold model of Bresnahan and

competitors as the key variable, we also ran

Reiss (1991). Standard Cournot oligopoly the-

regressions using the HHI. The results are

ory predicts that prices should initially fall

broadly similar to those reported. Thus the

quickly and then steadily approach marginal

assumption of identical firms does not signifi-

cost. A similar prediction is also provided by

cantly affect the empirical results.

Bresnahan and Reiss's entry threshold ratio

In our analysis N is the exogenous variable

method, which predicts a steady fall in variable

driving prices in equilibrium. We treat N as

profit margins. We compare the predictions of

this simple Cournot model to the alternative of

and other factors in the previous period or per-

a simple linear relationship between price and

iods, and price is then determined by the pre-

the number of sellers and to a more general

determined number of sellers in a particular

model that nests these alternatives.

consistent with the data and with previous

17. The coefficients on the HHI in the truncated regres-

research on the determinants of generic entry

sions are as follows (t-statistics in parentheses): for the

(see Scott Morton 1999; 2000). For example, a

whole sample, 0.003 (24.54); restricting the sample to

regression of N on sales in the year before

HHI ` 5,000, 0.001 (11.48); for HHI ` 3,000, 0.002

patent expiration (where data are available)

(5.214); for HHI ` 2,000, 0.005 (6.97); for HHI ` 1,000,

WIGGINS & MANESS: PRICE COMPETITION IN PHARMACEUTICALS

60% of variation of the number of sellers in the

postpatent period. Hence ex ante market size is

fixed effects provides a much richer set of con-

the key variable driving variation in N.

trols for cost and demand differences than the

It is also important to control for other fac-

existing literature. For example, Caves et al.

tors that might affect prices. One key factor is

(1991) consider products across therapeutic

possible competition from related products.

categories (such as cardiovasculars versus anti-

Ellison et al. (1997) found little evidence to

infectives) and simply use a single fixed effect

support such competition, and Stern (1994)

for anti-infectives, which is equivalent to

finds such effects in some categories. To control

imposing a restriction that all of the fixed

for these effects we included the number of

effects considered here are zero because the

other sellers in the appropriate broader cate-

entire data set consists of anti-infectives. Hence

goryofanti-infectives,suchaspenicillins,tetra-

the present study provides a large advance in

cyclines, and so forth. Brand recognition is also

the control of cost and demand factors in

important, and we included a dummy variable

studying pharmaceutical pricing relationships.

for versions of the same molecule sold by other

We used weighted least squares because the

innovative companies that had achieved brand

cells for different numbers of sellers had sharp-

ly different variances. We used as weights the

extensive analysis of branded, pioneer, and

inverses of the estimated standard deviation of

generic products. In contrast, different presen-

the residual for each value of the number of

tations of drugs do not differ sharply, except

competitors.20 The results from the estimation

injectable products are systematically more

are reported in Table 1. The results show

expensive to manufacture and distribute. We

general goodness of fit with a large F-statistic,

introduced an IV dummy to control for these

R2, and all of the key variables are highly

The model derived from equation (1) does a

differences that require fixed effects to control

good job of explaining the empirical relation-

for product age, product group, and year. Year

ship between price and the number of sellers of

of introduction fixed effects were included to

a given product. The results show that price is

control for differences in product age that

closely related to the inverse of the number of

could lead to differences in either demand

sellers of individual products, as predicted by

or cost. For example, physicians sometimes

the Cournot model. The parameter estimate for

use older products first in a course of therapy,

1/(N 1) is 28.70 with a t-statistic of 7.07. The

potentially affecting demand and price. Alter-

natively there may be a trend where manu-

declines when a firm loses its (patent-protected)

facturing costs of more recently developed

products are higher due to the more advanced

seller drops prices by nearly $5, the third by

nature of the products. Individual year of intro-

$2.39, the fourth by about $1.43, and the

duction fixed effects provide a flexible proce-

fifth by about $0.97. These price effects, more-

dure for accounting for such differences, and

over, are large relative to the mean price in the

we will compare the results of using such fixed

sample of $10.29. Hence, when there are more

sellers in a market the price falls sharply, but

In addition, products in different therapeu-

these price effects moderate quickly. Still, a

tic subcategories may differ in manufacturing

significant though small effect continues far

cost. Even though anti-infectives are generally

into the sample; going from 25 to 35 competi-

manufactured using similar techniques, there

tors is predicted to reduce prices in the struc-

could exist some differences across categories,

tural model by $0.31, or about 7.5%.

such as tetracyclines or penicillins. Accord-

It is worth noting several other results.

ingly, we include fixed effects for these groups.

Finally, fixed effects were included for individ-

economically and statistically significant

ual sample years to control for changes in

19. The data appendix provides summary statistics for

18. This information on brand names was obtained

from Scientific American Medicine. See section 3 for a

20. This method implies that separate weights are cal-

more complete investigation of our definition of brand

culated for each regression reported in the article. The

name and how brand name affects pricing and price

results were not qualitatively affected by using a common

set of weights, except as reported in the HHI regressions.

Regression Results Based on the Cournot Model

Notes: Dependent variable: real price per prescription. N number of sellers. NR number of sellers of related

products. HHI Herfindahl index. t-statistics are in parentheses. Real price is in 1982±84 dollars. Regressions are

weighted OLS. Weights are calculated by number of competitors and in each regression are equal to the standard

deviation of the residual for each number of competitors. An appendix, available from the authors, contains the fixed

coefficient for sellers of related products is

small, only 1.333, not quite significant at the

price of generic products in the sample is

95% confidence level. Hence, these data suggest

slightly more than $6, this variable indicates

that price effects are driven primarily by

changes in the number of sellers of the com-

pound in question, where we concentrate the

firmsÐover generics.21 The variable represent-

ing intravenous products also shows a substan-

Although we concentrate on sellers of indi-

tial price premium; the coefficient indicates

vidual chemicals, we do not interpret these

that such products are priced at $13.11 more

chemicals as being separate markets. Instead,

than other products, ceteris paribus.

we take the weaker position that taking the

number of sellers of related products into

pound in question (N ) has a large effect on

account makes little empirical difference.

price, the number of sellers of related com-

Hence it is appropriate to focus primary atten-

pounds (NR) has little effect. As noted, param-

tion on sellers of individual products.

eters predict a price decline of nearly $5 moving

Before turning to the other specifications it

is important to consider the fixed effects.23 The

number of sellers from two to three cuts prices

by another $2.50, and so forth. In contrast, the

22. Results with other specifications, such as using dif-

ferent functional forms for N and using the HHI in place of

the number of firms, yield broadly similar results.

21. The analysis in section III contains a more complete

23. A complete tabulation of regression results, includ-

ing the fixed effects, is available on request.

WIGGINS & MANESS: PRICE COMPETITION IN PHARMACEUTICALS

results show that only 9 of the 24 individual

indicate significant differences across subcate-

year of introduction fixed effects are statisti-

gories because a joint test restricting these

cally significantly different from the omitted

coefficients to zero is highly significant with

median (1973) at the 5% confidence level. How-

ever, an F-test reveals that these effects are

Finally, only three of the year fixed effects

jointly significant at the 1% level (F 14.38).

(1984±89) are significant at the 5% level.

Inspection of the coefficients shows that prior

Furthermore, there is no distinct trend in the

to 1973 all 11 are negative and after 1973 8 of 14

year coefficients, which indicates that the data

are positive. Nevertheless, there does not exist a

do not suggest a simple trend in price over the

simple trend in that there is considerable var-

iation in the individual year fixed effects over

The fixed effects show that it is important to

time, showing that this method provides a

control for cost and demand conditions. The

highly flexible method for accounting for pos-

rich set of fixed effects shows substantial non-

linear variation by year of introduction, and

there are generally small but significant differ-

included to control for vintage effects, such

ences in prices across subcategories. These

as increased quality for newer drugs, which

fixed effects provide a significant improvement

Lichtenberg (2001) demonstrates is an impor-

tant attribute of newer drugs relative to older

possible cost and demand differences. Hence

ones. To quantify these effects in a simple way,

the measured effect of competitors on price

we also ran the regression using an age variable

should not be the result of cost or demand

in place of year of introduction dummies. This

procedure also permits us to test whether our

Turning to the other specifications, an alter-

more general treatment of vintage effects mate-

native to the highly nonlinear, inverse specifi-

rially affected the results. Age is defined as

cation of column (1) of Table 1 is a linear

years since introduction of the chemical. We

relationship. To test between these specifica-

also include age squared to account for poten-

tions, one can nest the two models including

tial nonlinear vintage effects. This parametric

both the linear and nonlinear terms, as is done

treatment of age is more restrictive than the

in column (2) of Table 1. The results for the

nested model indicate that both terms are

constrains age effects to a quadratic form. The

significant, suggesting that prices fall faster

results, however, are essentially unchanged

than the simple Cournot-like model would pre-

for all the key variables. These results also

dict. Furthermore, although the linear terms

ensure that the specification of age effects

are significant, they are economically small.

does not account for any differences between

For example, as the second firm enters, the

the results here and those of other investiga-

primary model predicts a price decline of

tors. The estimate of the key coefficient on

about $5, whereas the nested model predicts

1/(N 1) in this specification is 37.18 with

a somewhat slower price decline of just over

a t-statistic of 8.97. The coefficient for age

$3; these differences are fairly small so that

is À0.461 with a t-statistic of À7.14. The

both models organize the data fairly well and

squared term is small, 0.007, with a t-statistic

of 5.70. For drugs that first entered the market

The most important difference between the

during our sample period, the average first-

year price is $54.41. The quadratic age effects

regards their prediction of price declines when

thus predict a fall in price of little more than

there are large numbers of firms. The nested

13% over 40 years ($7.14). This parametric

model predicts a larger price decline when there

approach suggests that systematic age effects

capture better the empirical phenomenon of

continuing price declines far into the sample.

fixed effects, we omitted the median fixed effect

In fact, the linear term is roughly the same

for trimethoprim (IMS class 15500). Of the

size as the coefficient in the simple regressions

20 fixed effects for individual product groups,

of price on N when the sample is restricted to

only 10 are statistically significantly different

more than 30 sellers; hence, the linear term in

from this median. Even though the number of

the nested model enables it to capture the con-

significant coefficients is small, the data do

tinuing price declines far into the sample.

Another difference occurs in the effect of

with t 4.816). Thus, removing other HHI

the number of sellers of related compounds.

from the primary regression does not alter

In the inverse specification, these sellers have

the results in any way. We also repeated the

a marginally significant effect, whereas in the

regressions in column (1) and (4) using the

nested specification, these products have a

log of price as the dependent variable.

statistically insignificant effect. The small size

The results are qualitatively unchanged.25

of these effects and their sensitivity to the

The price±N regressions and the price±HHI

specification may help explain the disparate

regression represent two competing linear

findingsofStern(1994)andEllisonetal.(1997).

The third column of Table 1 shows the sim-

ple linear model without the nonlinear term,

tests to determine which model best explains

and the results are similar. The model exhibits

the data. The results were inconclusive. One

large F-statistics and R2 as in the other two

method to test these nonnested alternatives is

specifications, and the coefficients of all

to create an artificial nested modelthat includes

explanatory variables are of the right sign

both (HHI and other HHI) and (1/[1 N ] and

and statistically significant. The key difference

1/[1 NR]) as independent variables along with

is that the linear model does not capture the

all the control variables and then conduct an

sharp initial price decline that characterizes

F-test on the HHI coefficients and the N coeffi-

cients (see Greene 1993, 222±23). The results

indicate that neither specification can be

initial entry on prices of these various thera-

rejected. The F-test that the coefficients on

peutic compounds. This relationship is present,

HHI and other HHI are both zero is 4.21. How-

moreover, both in a simple reduced-form anal-

ever, in this specification, the coefficient on

ysis and in an in-depth econometric analysis,

HHI is not statistically significant (0.00009,

where control is introduced for product age,

with a t-statistic of 1.19), and the joint signifi-

potential manufacturing cost differences, the

cance may be driven by the significance of the

number of sellers of closely related products,

(À0.0003, t-statistic À2.21). The test that

We also ran these regressions with HHIs in

1/(1 N) and 1/(1 NR) are simultaneously

zero is also easily rejected (F(2,3110)

regression is reported in the final column of

21.69). We also conducted a J-test of the two

Table 1. The results show a good fit, with an

competing models to ensure that the results

R2 of 0.808, slightly less than for the regressions

were not affected by the control variables

using number of sellers. The coefficient on the

(see Greene 1993, 223). Using the J-test, the

HHI for individual chemicals is positive and

hypothesis that the HHI model does not add

significant, indicating that decreasing concen-

any explanatory power cannot be rejected, and

tration does reduce price. The coefficient on

the HHI for the other chemicals in the IMS

model is easily rejected. Thus, the J-test

class is negative and significant, with a coeffi-

seems to favor using the inverse of the number

cient equal in size to that of its own chemical

of competitors as an independent variable over

entity, indicating that decreased concentration

in the broader class results in higher prices.

It is interesting to note the similarities and

differences between these results and those in

HHI regression (column [4]) with other HHI

prior work. Perhaps the most closely related

removed. The results were almost identical

work in the literature on the price±N relation-

to those reported in Table 1, column (4) (the

ship is Bresnahan and Reiss (1991). They exam-

coefficient in this regression was also 0.0004,

ine prices for dentists, auto repair shops, and

the like in geographically isolated county

seats. Their key finding was that the largest

competitive impact occurs moving from two

24. One limitation of the approach is that it imposes the

Cournot model. A second alternative is to construct a gen-

to three firms, another large impact moving

eral conjectural variations model which nests the Cournot

conjecture and let the data determine if the Cournot con-

jecture can be rejected. We constructed such a model and

found (using nonlinear least squares) that the Cournot con-

25. An appendix containing the results of this regres-

WIGGINS & MANESS: PRICE COMPETITION IN PHARMACEUTICALS

from three to four, and smaller subsequent

price impacts. They also argue that their

inferred prices in relatively concentrated

pricing by recognizing the differentiated nature

of generic and brand-name products. Brand-

The analysis here shows a sharp price drop

as the number of sellers increases from one to

consciouscustomers,andgenericfirmscompete

four or five and much smaller price effects

over price. Competition within and between

thereafter, similar to their finding. Bresnahan

these segments can provide insight into pricing

and Reiss also find a significant difference

patterns and permits testing of specific models

of competition between these groups.

(county seats) and unconcentrated (urban)

markets. Their finding is consistent with our

are two reasonable alternatives. One way is

results, which show a continuing price decline

to categorize the original patent-protected

product, defined hereafter as the pioneer, as

In contrast, the analysis here shows different

results from those found in previous research

products marketed by other innovative compa-

on pharmaceuticals. Studies by Caves et al.

nies that are separately promoted and have

achieved significant brand recognition even

though they are not the pioneer. We evaluate

entry. The results here show that pharmaceu-

both alternatives. To separate products with

tical prices respond to an increase in the num-

significant brand recognition, we categorized

ber of sellers similar to price responses found in

products specifically listed by brand name in

other markets.There are several possible expla-

the Scientific American Textbook of Medicine.

nations for these differences in results.

Theseproductsaregenerallydetailedtodoctors

Perhaps the most important is that the sam-

in varying degrees and may or may not differ

ple here is much larger than that used in these

from more traditional generic entry.

prior studies and contains much more variation

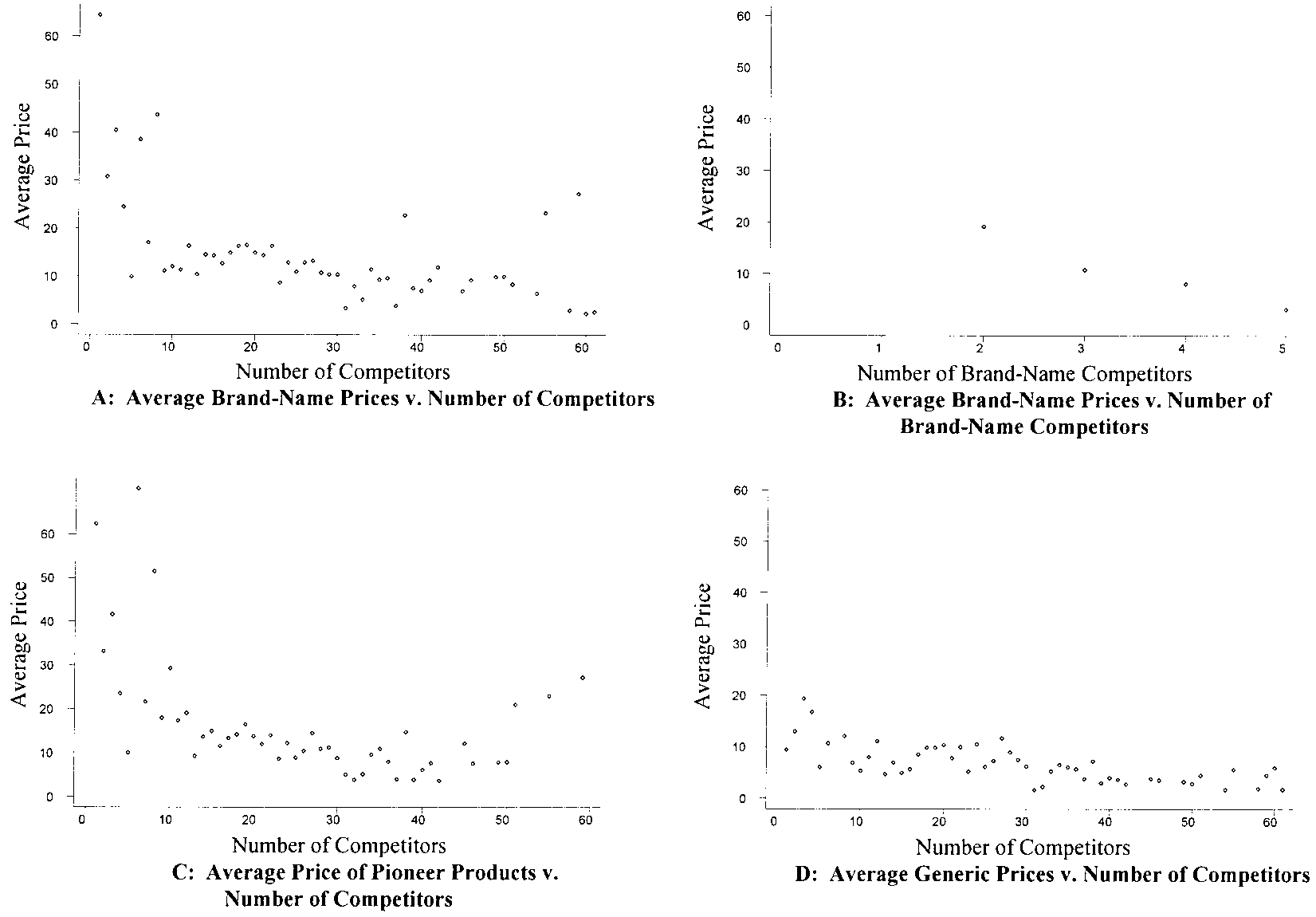

in the number of sellers. In addition, we do not

names, and generics leads to several reduced

restrict attention to a short period following

form relationships between price and N. We are

patent expiration but instead consider a variety

particularly interested in: (1) average brand-

of products with sharply different numbers of

name prices and the total number of sellers,

sellers. We also control more tightly for cost

(2) average brand name prices and the number

and demand differences. A different type of

of brand name sellers, (3) average prices of

possibility is that the analysis here focuses on

pioneer products and the total number of sell-

anti-infectives. Such a focus contributes to bet-

ers, and (4) average generic prices and the total

ter control for cost and demand differences, but

number of sellers. These relationships are illus-

comes at the cost of a more narrow focus. For

trated in the four panels of Figure 3. Panel A

example, by concentrating on anti-infectives,

shows the relationship between average brand-

the analysis focuses on products for which a

name prices and the total number of sellers of

single prescription is designed to cure, usage

a chemical. A shows that the price of brand-

patterns are similar, and underlying cost con-

name drugs falls steadily with the number of

ditions are likely more similar. These factors

competitors until there are roughly 25 to

improve the econometrics but of course mean

30 competitors; afterward the point estimate

that extrapolation to other therapeutic cate-

indicates continued price declines, but the

decline is no longer statistically significant.

Panel B of Figure 3 provides a different look

analyses of the price±N relationship and

at brand-name prices by showing how the aver-

prior studies of pharmaceutical pricing. The

age price of brand-name products is related to

omission is that it does not take into account

chemical.26 The data show a considerable but

unbranded products. We now turn to an expli-

irregular decline in price as the number of

cit analysis of the differentiated nature of

pharmaceutical products and the effect of

26. Note that care must be used in interpreting these

figures. For instance, the first point in B does not represent

brand name sellers rises. Panel C shows that

These data show that increases in the num-

prices of pioneers steadily decline as the num-

ber of sellers of individual chemicals leads to

ber of sellers of the chemical rises. This panel is

price decreases over a large range, but the pat-

a repeat of Figure 1B. Note that the price

tern of decrease and average price levels differ

decline exhibited here is much like that of

significantly for branded and generic products.

Figure 1A. Finally, D presents data on average

For generics significant price effects continue

generic prices as related to the total number of

far into the sample, whereas prices stabilize for

competitors. The results show that for generic

brand names when there are large numbers of

products prices fall steadily until there are more

metric analysis of the competition between

an average monopoly price because there may still be com-

petition from generic sellers even if there are no other brand

27. The coefficients for the number of competitors is as

It is common in the industry to view brand-

follows (t-statistics in parentheses): For brand-name

name products as being differentiated from

prices: N b 0, b À0.95 (À8.93), N ! 10, b À0.13

their generic competitors. Pricing patterns

(À3.84), N ! 20, b À0.12 (À2.62), N ! 30, b À0.03

after patent expiration and generic entry

(À0.38), N ! 40, b À0.02 (À0.13). For generic prices:

N b 0, À0.14 (À16.71); N ! 5, À0.12 (À14.17); N ! 10,

show that the price of the pioneer product

À0.12 (À13.78); N ! 20, À0.15 (À13.84); N ! 30 À0.07

remains much higher than the level of generic

(À4.40); N ! 40, À0.01 (À0.38). For the HHI regressions,

competitors for substantial periods of time. In

the coefficients are as follows. For brand names: overall,

b 0.006 (11.34); HHI ` 5,000, b 0.001 (2.88);

fact, previous empirical studies have found that

HHI ` 4,000, b 0.001 (1.873), HHI ` 3,000, b 0.002

prices of pioneer products tend to rise after

(1.584); HHI ` 2,000, b 0.004 (1.13). For generic prices:

overall, b 0.0006 (9.22), HHI ` 5,000, b 0.001 (10.72),

HHI ` 4,000, b 0.002 (9.20), HHI ` 3,000, b 0.002

(5.34), HHI ` 2,000, b 0.006 (7.23).

way to approach competition between branded

WIGGINS & MANESS: PRICE COMPETITION IN PHARMACEUTICALS

Notes: NG number of generic competitors. HHI Herfindahl index. t-statistics are in parentheses. Dependent

variable is real price is in 1982±84 dollars. Regressions are weighted OLS. Weights are calculated by number of

competitors and in each regression are equal to the standard deviation of the residual for each number of competitors.

Fixed effects dummy coefficients are not reported. Regressions only include cases where market has a single brand-name

seller and one or more generic sellers. Regressions are based on 565 observations meeting these conditions.

and generic products is to view them as differ-

than generic prices. Column (1) of Table 2

entiated products. In this setting, additional

reports the results of the first specification.

generic entry should have a larger impact on

The control variable coefficients are qualita-

tively similar to those in section II. The

because entry is taking place closer to existing

F-statistics and R2 are large. The primary coef-

generic competitors in product space.

ficients of interest in column (1) are the coeffi-

Table 2 presents several specifications of the

cient for the inverse of the number of sellers,

relationship between price declines for branded

and the variable interacting this variable with

and generic drugs. Because generic drugs are

brand name. The inverse of the number of sell-

likely to compete more closely with each other

ers has the incorrect sign but is not statistically

than with branded products, one might expect

significant. In contrast, the results show that

branded prices to fall more slowly than generic

generic entry lowers brand-name prices.

prices when additional generics enter. Such a

The second column in Table 2 reports a loga-

possibility is also consistent with some of the

rithmic specification, and the third reports a

empirical works described. To address this

linear specification. The final column in

issue in detail, we postulate several specifica-

Table 2 uses HHI in place of a functional

tions where one variable captures the overall

form based on the number of competitors.

price decline and a separate variable captures

All four specifications show a significant effect

the differential decline in the price of branded

of generic entry on brand-name prices but little

effect of generic entry on generic prices. The

The first column in Table 2 is derived from

result is that the analysis is that the data indi-

a formal model of spatial competition (see

cate faster price declines for brand names than

Wiggins and Maness 1998). The specification

generics, contrary to the conclusions of pre-

is very similar to the Cournot analysis. The

other specifications relax the highly specific

In addition, we examine several nonstruc-

functional form to test the qualitative result

tural alternatives. These models also permit

that brand-name prices should fall more slowly

Nested Nonspatial Models of Product Differentiation

Notes: Dependent variable price. NG number of generic competitors. NB number of brand-name competitors.

t-statistics are in parentheses. Dependent variable is real price is in 1982±84 dollars.

branded sellers affect prices, in addition to

the impact of generics on branded prices,

sell the incremental ``branded'' products (so-

called branded generics) in the sample. To

the extent that branded entry causes larger

model for a ``segmented market' in pharma-

price effects, the results indicate that branding

ceuticals with two groups, a loyal group of

leads to more effective price competition by

price-inelastic brand-name consumers and a

incrementally reducing prices in the branded

relatively price sensitive group of consumers.28

They argue there is little competition between

these segments. In such a case, the prices of

regressions investigating these hypotheses. A

brand-name products will be unaffected by

pooling test was conducted to see if the three

the number of generic competitors and, sym-

metrically, the number of brand-name sellers

respect to the effect of the number of sellers,

ought not affect generic prices. An alternative

and the results reject pooling. Subsequent pool-

view is that all products besides the original

ing tests were conducted for pooling pioneers

pioneer are generic. This view is implicit in

and other brand names and for generics and

much of the empirical literature, which gener-

brand names, and in each case pooling was

ally examines only the pioneer's prices, implic-

rejected. Accordingly the econometric results

itly treating all entry as generic.29 This

will analyze the separate effects of branded and

approach implies that pioneer products repre-

The regression results permit an in-depth

analysis of the nature of competition between

Our approach, in contrast, separates prod-

brand-name and generic sellers and the effect

on prices. In the brand-name price regression,

both brand name and generic entry affects

28. See also Grabowski and Vernon (1992). Frank and

Salkever (1997) provide empirical support for the segmen-

ted market hypothesis by demonstrating that branded

30. Due todatalimitations,theunreportedfixedeffects

prices tend to rise with generic entry while generic prices

discussed earlier are pooled across all three types, pioneer,

other brand name, and generic. To the extent that these

29. See, for example, Grabowski and Vernon (1992),

fixed effects represent cost and demand differences among

Caves et al. (1991), and Frank and Salkever (1997).

chemicals, this specification is correct.

WIGGINS & MANESS: PRICE COMPETITION IN PHARMACEUTICALS

prices, but the coefficient on brand-name

products is about ten times as large as the coef-

ficient on generic products and is the incorrect

This article has provided an empirical inves-

sign. Nevertheless, the results show significant

tigation of the relationship between price and

competition between these product groups,

the number of sellers in pharmaceuticals. The

analysis used a data set covering all anti-

market hypothesis and with the notion that

infective products and showed that initial

all sellers other than the pioneer should be

entry led to sharp price reductions, with prices

falling from the range of more than $60 per

Turning to the generic price equation, the

prescription for single sellers, $30 when there

results clearly indicate that generic firms do

are two or three sellers, and less than $20 when

respond to brand-name entry. Note, however,

there are four or more sellers. The results also

there are important differences in how generic

show that prices continued to decline with

prices respond to other generic as opposed to

additional entry, eventually approaching $4

brand-name entry. The linear term for generic

for products with more than 40 sellers.

entry is large and significant, whereas the

The results show that increases in the num-

inverse term is small and not significant. For

ber of competitors significantly reduce prices,

brand-name entry the response is similar, but

even when there are numerous sellers. These

the effect of brand-name entry on generic prices

results tie in nicely with those of Bresnahan

is substantially larger (À0.88 per brand-name

and Reiss (1991). Using small, isolated county

entrant versus À0.16 for an additional generic

seats, they find that the competitive effects of

entrant). The results once again show signifi-

entry diminish after the third or fourth entrant

cant competition between branded products

but that prices stabilize above those in uncon-

centrated urban markets. The results here show

The results for pioneer productsÐproducts

a similar, rapid initial price decline, and then go

sold by the original developerÐalso contrast

on to show a continuing steady decline as the

with the segmented market hypothesis.

number of sellers rises from a few to many.

Generic entry has a large and statistically sig-

nificant effect on pioneer prices, both for the

linear and nonlinear terms. Hence pioneer

observed pricing pattern. The analysis showed

products do indeed lower prices quite signifi-

prices broadly consistent with Cournot quan-

cantly in the face of additional generic com-

tity setting, though prices declined more with

petition.31 Furthermore, there is suggestive

large N than that model would predict.

The analysis also ties into the emerging work

entry also effects pioneer prices in that the

on pharmaceutical prices. The analysis here has

linear term is quite large and statistically sig-

extended that work in several directions. One

nificant, although the inverse of the number of

direction is to provide a much more compre-

brand-name sellers has the wrong sign.

hensive analysis of pricing in a specific, impor-

Hence the results support the argument that

tant therapeutic category. Our results show

there is significant competitive interaction

substantial price sensitivity and stand in

contrast to results found by Caves et al. and

firms. These results indicate considerable com-

Grabowski and Vernon. There are several pos-

petition and show that increases in the number

sible reasons for these differences. One is that

of sellers in any segment generally reduce prices

the analysis here relied on all anti-infectives,

in the remaining segments. This competition

not restricting attention to the period closely

following patent expiration. The greater varia-

tion in the number of sellers also provides a

richer data set particularly because the analysis

used data exclusively since 1984, when there

were large numbers of generic sellers. This

31. There are several possible reasons for these differ-

ences from Grabowski and Vernon. Perhaps the most

important is that we have a much larger sampleÐthey con-

Waxman-Hatch Act, which eased the burdens

sidered only 18 products. It is also possible that their results

of generic entry. A second possible reason is

are confounded due to difficult to control for cost differ-

ences, or that our results are special due to the differential

that anti-infectives may be more price-sensitive

than other segments of the pharmaceutical

industry. This possibility, of course, means

Brookings Papers on Economic Activity: Microeco-

that one must be careful in drawing inferences

from this analysis to pharmaceuticals more

Congressional Budget Office. How Increased Competition

from Generic Drugs Has Affected Pricesand Returns in

the Pharmaceutical Industry. July 1998.

The analysis also provided an econometric

Dunne, Timothy, and Mark J. Roberts. ``Costs, Demand,

investigation of differentiated product models

and Imperfect Competition as Determinants of Plant-

by treating brand-name and generic products

Level Output Prices.'' Manuscript, Department of

as differentiated. The problem is to explain

Economics,PennsylvaniaStateUniversity,December

the persistent price difference between brand-

Ellison,SaraF. ``WhatPricesCanTellUsabouttheMarket

name products and their generic competitors.

for Antibiotics.'' Working Paper, MIT, July 1998.

The results indicate that a general spatial

Ellison, Sara F., Iain Cockburn, Zvi Griliches, and Jerry

model of product differentiation does not

Hausman. ``Characteristics of the Demand for Phar-

adequately explain pricing behavior in the

maceutical: An Examination of Four Cephalospor-

ins.'' Rand Journal of Economics, 28(3), 1997, 426±46.

pharmaceutical industry because brand-name

Frank, Richard G., and David S. Salkever. ``Pricing, Patent

products respond aggressively to generic entry.

Loss and the Market for Pharmaceuticals.'' Southern

The results, however, also reject the segmented

Economic Journal, October 1992, 165±79.

market hypothesis, showing instead that there

ÐÐÐ. ``Generic Entry and the Pricing of Pharmaceuti-

is important competition between the pioneer,

cals.'' Journal of Economics & Management Strategy,

brand name, and generic segments. Multiple

Grabowski, Henry G., and John M. Vernon. ``Brand Loy-

alty, Entry and Price Competition in Pharmaceuticals

there are important differences in the compet-

afterthe1984DrugAct.''JournalofLaw&Economics,

itive effects of additional branded entry com-

pared to the effects of incremental generic

ÐÐÐ. ``Longer Patents for Increased Generic Competi-

Decade.'' PharmacoEconomics, 10(suppl 2), 1996,

firms, there is a significant inverse relationship

between price and the number of competitors,

Greene, William H. Econometric Analysis, 2nd ed. New

whether those competitors are brand name or

Griliches, Zvi, and Iain Cockburn. ``Generics and New

Goods in Pharmaceutical Price Indexes.'' American

The broad implication of the analysis is that

Economic Review, 84(5), 1994, 1213±32.

entry of additional sellers reduces prices much

Lichtenberg, Frank R. ``Are the Benefits of Newer Drugs

more substantially than previous work would

Worth Their Cost? Evidence from the 1996 MEPS.''

suggest. The extent to which these results carry

Health Affairs, September/October 2001, 241±51.

over to other therapeutic classes remains an

Lu, Z. John, and William Comanor. ``Strategic Pricing

of New Pharmaceuticals.'' Review of Economics and

Statistics, 80, February 1998, 108±18.

Masson, Alison, and Robert L. Steiner. Generic Substitu-

tion and Prescription Drug Prices: Economic Effects of

State Product Selection Laws. Washington, DC: Fed-

Applebaum, E. ``The Estimationof theDegree ofOligopoly

Power.'' Journal of Econometrics, 19, 1982, 287±99.

Porter, R. ``A Study of Cartel Stability: The Joint Executive

Bresnahan, T. F. ``Departures from Marginal-Cost Pricing

Committee, 1880±1886.'' Bell Journal of Economics,

in the American Automobile Industry: Estimates for

1977±1978.''JournalofEconometrics,11,1981,201±27.

Reiffen, David, and Michael R.Ward. ``Generic Drug

ÐÐÐ. ``Empirical Studies of Industries with Market

IndustryDynamics.'' WorkingPaper, FTC,February

Power,'' in The Handbook of Industrial Organization,

edited by R. Schmalensee and R. Willig. North-

Reiss, Peter C., and Pablo T. Spiller. ``Competition and

Entry in Small Airline Markets.'' Journal of Law &

Bresnahan, T. F., and P. C. Reiss. ``Entry and Competition

Economics, 32, October 1989, S179±S202.

in Concentrated Markets.'' Journal of Political Eco-

Schmalensee, Richard. ``Entry Deterrence in the Ready-to-

Eat Breakfast Cereal Industry.'' Bell Journal of

Caves, Richard E., Michael D. Whinston, and

Mark A. Hurwitz. ``Patent Expiration, Entry and

Schwartzman, David. Innovation in the Pharmaceutical

Competition in the U.S. Pharmaceutical Industry.''

Industry. Baltimore, MD: Johns Hopkins University

Scientific American Medicine. Edited by Edward Rubin-

32. Reasons for such caution include possible cost and

stein and Daniel Federman. New York: Scientific

regulatory differences, the fact that a single prescription is

often part of a maintenance program of therapy in other

Scott Morton, Fiona M. ``Entry Decisions in the Generic

pharmaceutical areas, and such repeated use may lead to

PharmaceuticalIndustry.''RandJournalofEconomics,

differences in brand loyalty and competition.

WIGGINS & MANESS: PRICE COMPETITION IN PHARMACEUTICALS

Scott Morton, Fiona M. ``Barriers to Entry, Brand Adver-

Suslow, V. ``Estimating Monopoly Behavior with Compe-

tising, and Generic Entry in the US Pharmaceutical

titive Recycling: An Application to Alcoa.'' Rand

Industry.'' International Journal of Industrial Organi-

Journal of Economics, 17(3), 1986, 389±403.

Wiggins, Steven N., and Robert Maness. ``Price Competi-

Stern, Scott. ``Product Demand in Pharmaceutical

tion in Pharmaceutical Markets: The Case of Anti-

Markets.'' Mimeo, Sloan School of Management,

infectives.'' Working Paper, Texas A&M University,

now an open secret that this ‘resolve’more illusory. Not only the litigation isally takes around 20 yearsin getting one single casedecided. As a result of thisthe present justice deliv-ery system is beyond themeans of the commoncourts of law for gettingjustice. Masses shy away togo to the courts for gettingjustice and rather prefer to THE CHARTERED ACCOUNTANT DECEMBER 2004

3018992 CARLYTENE 30 MG (MOXISYLYTE), 32 comprimés enrobes3019454 CELESTAMINE (bétaméthasone, dexchlorphéniramine), comprimés (B/30)3045411 GLYCO-THYMOLINE 55, solution buccale, 250 ml en flaconDIVERS stomato local (antiinfectieux ou antiseptiques)3051222 HYDERGINE 1 MG/ML (MESILATE DE DIHYDROERGOTOXINE), 1 Flacon de 50 ml avec mesurette graduée, solution buvable en gouttes,3054255 ISKE

The average branded price (constant dollars) is

$30.30 with a standard deviation of $45.77, and

the average generic price (constant dollars) is

$6.27 with a standard deviation of $6.91. The

number of sellers for a given product varies

from 1 (monopoly) to 61. The mean is 26.9

sellers. Our measure for the number of related

sellers has a mean of 31.6 and ranges between

0 and 112. We also calculated the Herfindahl

entity in each year. The mean HHI in the sam-

ple is 3,677, and the standard deviation is 2,669.

The average branded price (constant dollars) is

$30.30 with a standard deviation of $45.77, and

the average generic price (constant dollars) is

$6.27 with a standard deviation of $6.91. The

number of sellers for a given product varies

from 1 (monopoly) to 61. The mean is 26.9

sellers. Our measure for the number of related

sellers has a mean of 31.6 and ranges between

0 and 112. We also calculated the Herfindahl

entity in each year. The mean HHI in the sam-

ple is 3,677, and the standard deviation is 2,669. WIGGINS & MANESS: PRICE COMPETITION IN PHARMACEUTICALS

Prices of Products and Number of Competitors

range. B, focusing just on the prices of the pio-

continuing price decline in the reduced form

neer developer, shows essentially the same

that continues from only a few sellers to more

pattern. Hence, these data show a decline in

than 40. Focusing just on the pioneer pro-

both overall average prices and prices of the

We tried other specifications, and all the

The continuing price decline is well illus-

results are broadly similar. For instance,

trated through a series of simple regressions of

although our analysis concentrates on the

the price±N relationship, with progressive

price±N relationship, we also calculated

truncation of the sample on N from the left-

the HHI for each of our 98 chemicals. The

hand side. These regressions permit one to

mean HHI was 3,677 with a standard deviation

assess the persistence of the inverse relation-

of 2,669. The range was 1,082 to 10,000. After

ship between price and N. The results show

constructing the HHI, we then replicated the

that there is a statistically significant impact

regressions using the HHI in place of the num-

of the number of sellers on price, including

ber of firms. We ran a series of regressions,

when the sample is restricted to more than

30 sellers.15 Hence there is a significant,

16. It should be noted that there is a single outlier for

the pioneer products, which makes some difference in the

15. The coefficient on the number of sellers in the sim-

results. There appear to be data problems with the prices

ple price±N truncated regressions are as follows (t-statistics

for this drug, Vibramycin (PFizer: the pioneer doxy-

in parentheses): for regressions including all chemicals

cycline). If Vibramycin is included, the effect of N is insig-

(N b 0), b À0.47 (À21.42); for the regressions including

nificant for N ! 20, and significant and positive for N ! 30.

WIGGINS & MANESS: PRICE COMPETITION IN PHARMACEUTICALS

Prices of Products and Number of Competitors

range. B, focusing just on the prices of the pio-

continuing price decline in the reduced form

neer developer, shows essentially the same

that continues from only a few sellers to more

pattern. Hence, these data show a decline in

than 40. Focusing just on the pioneer pro-

both overall average prices and prices of the

We tried other specifications, and all the

The continuing price decline is well illus-

results are broadly similar. For instance,

trated through a series of simple regressions of

although our analysis concentrates on the

the price±N relationship, with progressive

price±N relationship, we also calculated

truncation of the sample on N from the left-

the HHI for each of our 98 chemicals. The

hand side. These regressions permit one to

mean HHI was 3,677 with a standard deviation

assess the persistence of the inverse relation-

of 2,669. The range was 1,082 to 10,000. After

ship between price and N. The results show

constructing the HHI, we then replicated the

that there is a statistically significant impact

regressions using the HHI in place of the num-

of the number of sellers on price, including

ber of firms. We ran a series of regressions,

when the sample is restricted to more than

30 sellers.15 Hence there is a significant,

16. It should be noted that there is a single outlier for

the pioneer products, which makes some difference in the

15. The coefficient on the number of sellers in the sim-

results. There appear to be data problems with the prices

ple price±N truncated regressions are as follows (t-statistics

for this drug, Vibramycin (PFizer: the pioneer doxy-

in parentheses): for regressions including all chemicals

cycline). If Vibramycin is included, the effect of N is insig-

(N b 0), b À0.47 (À21.42); for the regressions including

nificant for N ! 20, and significant and positive for N ! 30.

brand name sellers rises. Panel C shows that

These data show that increases in the num-

prices of pioneers steadily decline as the num-

ber of sellers of individual chemicals leads to

ber of sellers of the chemical rises. This panel is

price decreases over a large range, but the pat-

a repeat of Figure 1B. Note that the price

tern of decrease and average price levels differ

decline exhibited here is much like that of

significantly for branded and generic products.

brand name sellers rises. Panel C shows that

These data show that increases in the num-

prices of pioneers steadily decline as the num-

ber of sellers of individual chemicals leads to

ber of sellers of the chemical rises. This panel is

price decreases over a large range, but the pat-

a repeat of Figure 1B. Note that the price

tern of decrease and average price levels differ

decline exhibited here is much like that of

significantly for branded and generic products.